HH Investment set a $1,820 psf ppr record at Bukit Timah Road in November 2025 — the second-highest GLS land rate in Singapore history and 13% above UOL/SingLand's Orchard Boulevard bid. The 1H2026 GLS Confirmed List offers 4,575 units across nine plots, roughly 10% fewer units than the previous programme. Bayshore Drive (1,280-unit integrated, analysts expect up to $2B tender) and New Upper Changi Road (1,040 units, first Bedok Central GLS in 15 years) are the two plots most likely to define OCR launch benchmarks when they hit market in late 2027 or 2028.

Sources: URA, EdgeProp, The Edge Singapore, PropNex, Huttons, Stacked Homes, 99.co

The two-speed market nobody quite believes yet

2025 closed with new launches selling out at 80-90% on opening weekend. The pattern held across CCR, RCR, and OCR: even half-decent projects were clearing fast. At the same time, resale units in some of Singapore's best-known developments have been sitting on the market for three, four, even five months.

On the surface it reads like a contradiction. If new launches are this hot, why is resale stuck?

The answer is that the two segments are now running on different clocks. New launches are being priced against future land cost projections, projections that the 1H2026 Government Land Sales slate has just reinforced. Resale sellers are chasing the same numbers, but without the developer marketing engine that actually gets those prices paid. And hanging over both segments is a land cost trajectory that keeps writing new records: the Bukit Timah Road GLS site sold in November 2025 at $1,820 psf ppr, the second-highest land rate in Singapore GLS history.

If you are shopping right now, the entire 1H2026 picture is telling you one thing: the floor keeps rising, supply is being compressed, and "waiting for prices to come off" is not a strategy the last five years have rewarded.

How we review: the QPE framework

Every review on this site runs through our QPE framework: Quality, Exit, Price.

Quality covers developer track record, land size, layouts, MRT access, views, and facilities. Exit asks who buys from you when it is time to sell, what the demand pool looks like, and what competing supply exists at resale. Price examines total price (not psf) and how it compares against what the market has tested: is there a price gap, or are you paying above proven territory?

All three need to check out. If one fails, you need to know which one — and why.

Why resale actually moves slower (and it is not because resale is cheap)

The standard explanation for the resale slowdown is that buyers are all chasing new launches. That is part of the picture, but it misses the bigger mechanism.

Resale asking prices are at all-time highs in most segments. Skyline Residences owners are calling for $2.8 million-plus on their 1,055 sqft stacks, prices that still sit below the per-square-foot rates at The Pen, but easily $200,000-$300,000 above where the same units were trading a year ago. D'Leedon 4-bedroom resale transactions have touched $4.15 million in the past few months, against $3.3-3.5 million for comparable units in the first half of 2025. The demand is there. What is missing is the speed at which buyers can emotionally process a 15-20% upward reset on resale pricing.

The same inflation shows up in smaller condos. Resale listings in mature freehold estates are routinely asking 8-12% more than comparable transactions from 12 months ago. The transactions are still happening, but the matching process is slower because every buyer now needs to cross-check recent URA data, land cost trends, and new-launch pricing to figure out whether an asking price is grounded or ambitious.

Here is the part that gets missed. The resale market is not stuck because it is expensive. It is stuck because owners have raised their asking prices in response to new launches, but they do not have developer launch weekends, showflat marketing, or staged releases to force-match demand. Good units at realistic asking prices still move. Average-layout units with sky-high asking prices take months.

For buyers, that actually creates an opportunity. If you are patient, the resale market rewards picking: finding motivated sellers, units with clean layouts in proven developments, and owners who understand that the all-time high on paper is not the same as the transactable price. The overall resale trend stays elevated, and yet individual deals inside that trend routinely land 5-8% below the cluster average if you are willing to walk the developments yourself.

The $1,820 PSF PPR Bukit Timah Road record: what it actually signals

The headline number from late 2025 was the Bukit Timah Road GLS tender. HH Investment, a developer with Taiwanese roots that most local buyers have never heard of, outbid seven other parties with a top offer of $566.292 million, working out to $1,820 psf per plot ratio.

That is the second-highest land rate in Singapore GLS history for a residential plot. And it landed on a relatively compact site in the Newton neighbourhood, near ACS (Junior) and the Newton MRT interchange.

Here is how recent CCR and prime GLS results compare:

| GLS Site | Developer | Year | Land Rate (psf ppr) |

|---|---|---|---|

| Orchard Boulevard (UpperHouse) | UOL / SingLand | Feb 2024 | $1,616 |

| Zion Road (Parcel A) | CDL / Mitsui Fudosan | Apr 2024 | $1,202 |

| Zion Road (Parcel B) | Allgreen Properties | Jul 2024 | $1,304 |

| Holland Link | Sim Lian JV | Aug 2025 | $1,432 |

| Telok Blangah Road | Kingsford Group | Late 2025 | $1,326 |

| Bukit Timah Road (Newton) | HH Investment | Nov 2025 | $1,820 |

| Lentor Central | GuocoLand / Intrepid / TID | Mar 2026 | $1,278 |

The Orchard Boulevard comparison is the interesting one. UOL and SingLand paid $1,616 psf ppr for the Orchard Boulevard plot in February 2024, a plot that is directly linked to the Orchard Boulevard MRT station on the Thomson-East Coast Line, sitting inside the single most prestigious residential address in Singapore. That project is now selling as UpperHouse at Orchard Boulevard, and moved 53% of units on launch day at an average of $3,350 psf.

The Newton plot came in at 13% above Orchard Boulevard. If Orchard Boulevard launched at $3,350 psf, then a Newton CCR project on land that cost 13% more is looking at theoretical launch pricing well above $3,700-$3,800 psf, and that is before factoring in the premium HH Investment is likely to push for to justify the aggressive bid.

Running our shortcut on the Bukit Timah Road bid: $1,820 x 2.23 = approximately $4,059 psf as a theoretical launch reference. Even allowing for softening margins, anything under $3,800 psf at launch would be surprising.

The Newton number matters beyond its own plot because it sets a ceiling reference for every other CCR developer pricing land right now. When you are bidding for a prime district site in early 2026, $1,820 psf ppr is the number you know exists, and the number you need to justify not exceeding.

The Peck Hay Road site on the 1H2026 Confirmed List will be the first real test. It sits in the same Newton neighbourhood, it is also a compact CCR plot, and it is already attracting interest from luxury-focused developers. Our Peck Hay Road GLS preview tracks the tender setup. The expected bid range lands somewhere between $1,600 and $1,700 psf ppr, though if competitive intensity matches Bukit Timah Road, we could see that ceiling challenged again.

1H2026 GLS: nine plots, 4,575 units, and 10% less supply

The 1H2026 Confirmed List landed in late 2025 with nine sites: six private residential plots, two executive condominium plots, and one mixed-use commercial-and-residential integrated development. Together they can yield 4,575 private residential units, including 635 EC units, alongside roughly 242,188 sqft of commercial gross floor area.

The previous programme carried 5,030 units. The 1H2026 number is approximately 10% lower. That reduction is deliberate, and worth thinking about alongside the bidding intensity we saw in late 2025. Less supply plus stronger take-up means more aggressive land bidding, which feeds directly into higher launch prices, which feeds into the resale reference pool, the cycle the market has been in since 2022.

| Site | Land Size | Est. Units | Plot Ratio | Key Feature |

|---|---|---|---|---|

| Bayshore Drive (Integrated) | 5.74 ha | 1,280 | 2.6 | Mega mixed-use, direct MRT, ~242k sqft commercial GFA |

| New Upper Changi Road | 3.16 ha | 1,040 | 2.8 | First Bedok Central GLS in ~15 years |

| Berlayar Drive | 2.54 ha | 415 | 1.44 | Second plot at former Keppel Club, GSW, sea-fronting potential |

| Peck Hay Road | 0.55 ha | 315 | — | CCR, next to Newton MRT, near ACS (Junior) |

| Holland Plain | 1.57 ha | 280 | — | Second plot in the Holland Plain precinct |

| River Valley Green (Parcel SE) | ~1.15 ha | ~240 | — | Sandwiched between Yong An Park and River Modern |

| Lorong Puntong | ~0.43 ha | 140 | — | Smallest site. Opposite Bright Hill MRT and Ai Tong School |

| Canberra Drive (EC) | ~1.14 ha | 185 | — | Near Canberra MRT. Behind Brownstone and Visionaire |

| Sembawang Drive (EC) | — | ~450 | — | Furthest EC site, limited nearby amenities at launch |

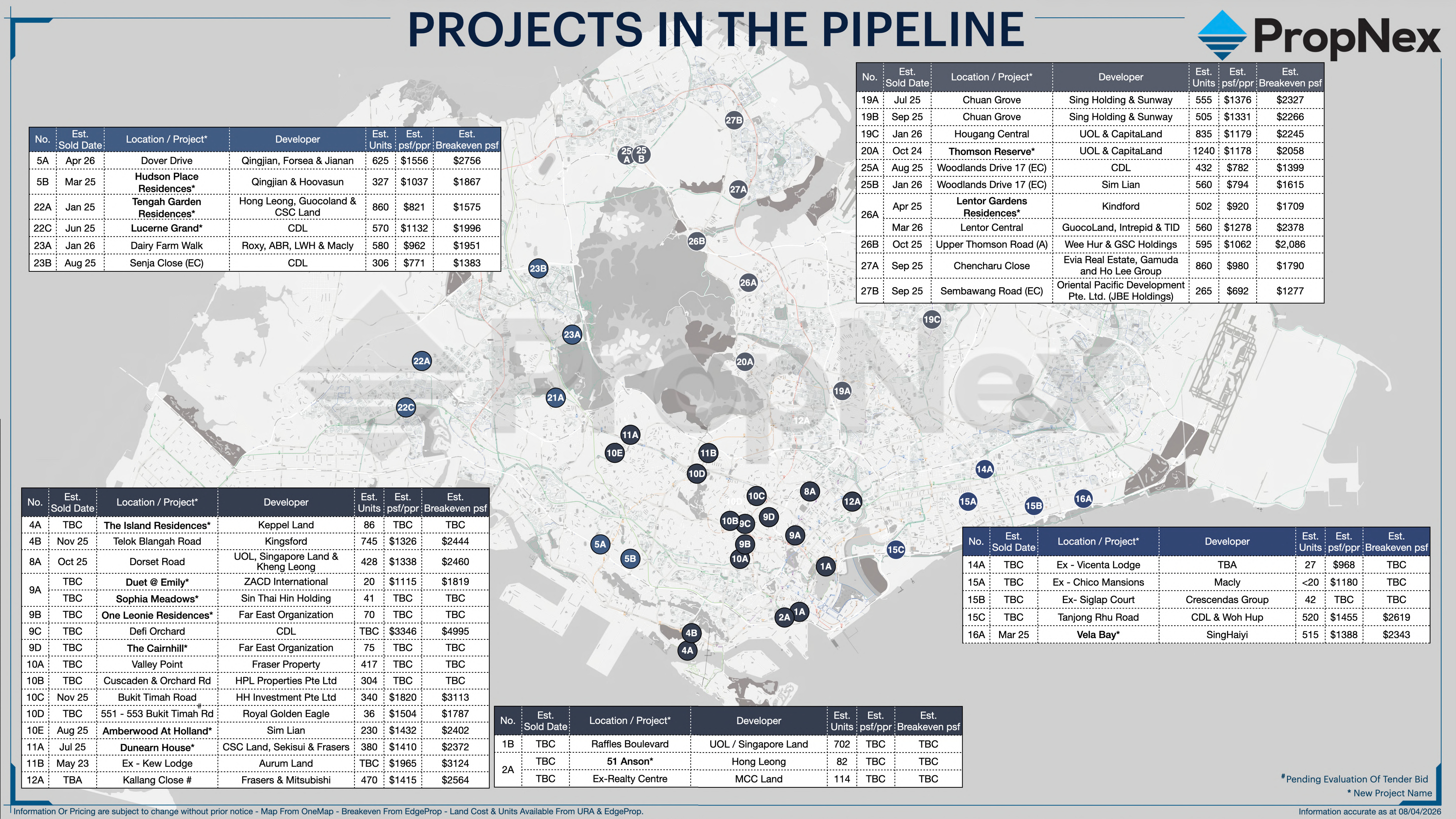

The 1H2026 slate does not sit in isolation. It lands on top of an already crowded new-launch pipeline: mature estates, CCR pockets, ECs, en bloc replacements. PropNex's projects-in-the-pipeline map is the cleanest single view of what is actually coming to market across the next 18-24 months.

Source: PropNex Projects in the Pipeline (8 April 2026)

Not every site is a blockbuster. Three of them (Bayshore Drive, New Upper Changi Road, and Berlayar Drive) are what analysts are calling the headline plots. Another three (Peck Hay Road, Holland Plain, Lorong Puntong) are solid but situational. The remaining three (River Valley Green, Canberra EC, Sembawang Drive EC) are routine additions, useful, but unlikely to set any benchmarks.

The cluster that matters most is the headline three. Each carries a different buyer pool, a different location profile, and a different implication for 2027 launch pricing.

Bayshore Drive: the mega site that could draw a $2 billion bid

The Bayshore Drive integrated site is the largest plot in the 1H2026 slate, and arguably the most ambitious residential GLS tender of the last decade. 5.74 hectares. 1,280 estimated units. Roughly 242,188 sqft of commercial gross floor area. A plot ratio of 2.6, which could yield towers of around 30 storeys depending on height restrictions near Changi Airport flight paths.

The location is the point. Bayshore MRT sits on the Thomson-East Coast Line and opened in June 2024. The precinct is part of the Long Island coastal protection and rejuvenation project, a long-term government plan to add reservoirs, parks, and additional reclaimed land along the entire eastern coast. And the site has direct access to the sea view on the southeastern side, something that no OCR plot of comparable size can match.

The Edge Singapore and Huttons have both floated estimates that the Bayshore Drive tender could draw bids in the region of $2 billion, which would translate to a land rate around $1,450-$1,500 psf ppr for an integrated development. SingHaiyi's earlier $1,388 psf ppr top bid on the first Bayshore plot was a standalone residential parcel, meaning the integrated version should command a premium given the commercial component and the sheer scale.

Running the shortcut formula: $1,450 x 2.23 = approximately $3,234 psf as theoretical launch pricing. Real integrated developments typically launch at a slight premium to that: mixed-use construction is more expensive, and the retail component has to be priced separately. A launch range of $3,100-$3,300 psf for the residential portion would not surprise us.

For buyers already tracking the east side, this is the plot to monitor. Our Bayshore Drive GLS preview has the ongoing research. Tender closes July 15, 2026. Launch, realistically, falls in late 2027 or early 2028.

New Upper Changi Road: Bedok's quietly huge moment

If Bayshore Drive is the most talked-about plot, New Upper Changi Road is the one most likely to define OCR launch pricing for the next buying cycle.

The site sits at 2 Bedok South Road, 3.16 hectares, plot ratio 2.8, yielding an estimated 1,040 units across what is expected to be 21-23 storey blocks. It is the second-largest residential GLS plot in the 1H2026 slate, and more importantly, it is the first new private GLS release within walking distance of the Bedok integrated transport hub in roughly 15 years.

Bedok sits in a different tier than Newton, Orchard, or Marina Bay, and that is exactly the point. It is one of the most mature HDB estates in Singapore, and upgraders from the surrounding flats have been without a credible new launch option for most of the last decade. You can see the pent-up demand in how quickly any Bedok resale listing with a clean layout clears the market. Opera Estate Primary School sits within 500 metres, anchoring the family buyer pool. Bedok MRT, Bedok Mall, and the Bedok Hawker Centre are all within walking distance. And on the higher floors facing southeast, there should be unblocked sea views past the landed housing at the front of the plot.

The buyer mix is the interesting part. A 1,040-unit OCR plot near Bedok MRT pulls from three pools at once: HDB upgraders from Bedok, Chai Chee, and Kembangan; private downgraders from the surrounding landed Opera Estate, Siglap, and Frankel Estate neighbourhoods; and the normal investor pool targeting East Coast condos. That demographic overlap is exactly what makes OCR mega-sites work when the fundamentals line up.

Analyst expectations place the expected bid range around $1,400-$1,450 psf ppr. Running the formula: $1,400 x 2.23 = approximately $3,122 psf as a theoretical launch reference. For a 900 sqft 3-bedroom unit, that translates to roughly $2.81 million at the benchmark, a number that may look aggressive today but will likely feel normal by the time the project actually launches in late 2027 or early 2028.

Our full New Upper Changi Road GLS analysis tracks the plot details. For anyone already considering east-side buying, this is the plot to benchmark against.

Berlayar Drive: the first sea-fronting plot at the Greater Southern Waterfront

The Berlayar Drive plot is the second site on the former Keppel Club land to come up for sale as part of the Greater Southern Waterfront precinct. The first was the Telok Blangah Road parcel that Kingsford Group won last year at $1,326 psf ppr. Berlayar Drive sits closer to the sea, with views across to Sentosa and the southern shoreline.

2.54 hectares. 415 estimated units. Plot ratio of 1.44, deliberately low-density, which means whatever developer wins this site will be building a project with more land per unit, lower floor counts, and a layout style closer to Caribbean at Keppel Bay or Corals at Keppel Bay than to a typical OCR mega-development.

The challenge with the Greater Southern Waterfront has always been local demand depth. Harbourfront, Telok Blangah, and Keppel Bay are prestigious addresses, but the family buyer pool is thinner than in mature OCR estates like Bedok or Tampines. That said, the precinct-level rejuvenation has real backing. The government has committed to transforming the entire stretch from Keppel to Marina South over the next 15-20 years, with new parks, residential precincts, and MRT connectivity. For buyers who want early positioning in a long-term rejuvenation play, this is one of the few plots offering it.

The expected bid range sits around $1,350-$1,400 psf ppr, which would translate to roughly $3,010-$3,122 psf at launch. For a project with sea views and low-density design, that is competitive with comparable low-density plots in other CCR-edge zones. If you are someone who values quieter, lower-rise living with water views, this plot is worth watching. If your priority is MRT doorstep access and school cluster depth, the Bedok plot or the Bayshore integrated site will serve you better.

The smaller plots that still deserve attention

Peck Hay Road is the CCR compact plot, 0.55 hectares, 315 units, next to Newton MRT interchange. It sits in the same neighbourhood as the $1,820 psf ppr Bukit Timah Road record, which means any developer bidding for this site has to reference a very aggressive recent comparable. ACS (Junior) within 1km is the school anchor, and the plot is small enough that a luxury developer is likely to focus on larger unit sizes rather than maximising unit count. Our Peck Hay Road GLS preview is tracking the tender setup. Expected bid range $1,600-$1,700 psf ppr, but the Bukit Timah Road result means anything higher would not shock the market.

Holland Plain is the second plot in the Holland Plain precinct, 1.57 hectares, 280 units. Sim Lian paid $1,432 psf ppr for the adjacent Holland Link plot in August 2025, and analyst expectations for this new plot land somewhere between $1,350 and $1,500 psf ppr. The location is pleasant, Holland Village MRT is a short drive, and the buyer pool skews toward upgrader families who specifically want the Holland Village lifestyle. If you are someone who cares about that specific neighbourhood, this will be the only CCR-edge option in the precinct for a while.

Lorong Puntong is the smallest plot in the slate, approximately 0.43 hectares yielding just 140 units. It sits directly opposite Bright Hill MRT on the Thomson-East Coast Line and across the road from Ai Tong School. Huttons estimates up to 10 bidders and a top bid around $180 million. Expected land rate comes in below $1,350 psf ppr. For young families anchored on Ai Tong School access, this is the only nearby GLS plot that delivers that specific advantage in the next two years. Boutique-scale, family-focused, and likely to move quickly at launch. The nearby Thomson View en bloc redevelopment (1,240 units, same TEL corridor) will likely launch before this one, which could influence pricing dynamics; our rising land costs commentary has the longer-form read on that corridor.

River Valley Green Parcel is the one plot most likely to be dragged down by competition. It sits sandwiched between Yong An Park and River Modern, in a micro-market that has already absorbed multiple recent launches. The view options are limited: the north faces Yong An Park, the east faces River Valley Primary School, and the south overlooks River Modern. That said, River Valley as a precinct remains a premium CCR-edge location, and any plot here will clear eventually. Expected land rate around $1,450-$1,500 psf ppr.

Canberra Drive (EC) and Sembawang Drive (EC) are the two executive condominium plots. Canberra is tucked behind Brownstone and Visionaire with 185 units, a routine addition to the estate. Sembawang Drive sits further out from core amenities and leans on the long-term Sembawang shipyard transformation case. Both plots will absorb first-time HDB upgrader demand, but neither is positioned to be a benchmark-setter. Expected land rates around $650-$680 psf ppr.

The quieter squeeze: supply down, en bloc rules under review

The headline number from the 1H2026 Confirmed List is 4,575 units, which is 10% below the prior programme. But there is a second supply-side shift running alongside it that most buyers have not priced in yet.

The government has reportedly been reviewing the collective sale (en bloc) threshold rules. Under current regulations, at least 80% of unit owners in a development must agree before an en bloc sale can proceed. The proposed change would lower that threshold to 70%. If the revision goes through, and there is no official confirmation yet, a meaningful number of aging developments that have been stuck in the 70-80% range could suddenly clear the bar.

Think about what that would mean. Less state land supply through GLS, combined with more private land coming to market through en bloc sales, shifts the redevelopment pipeline toward private collective deals. Developers still need to replenish their land banks. If they cannot find enough through GLS, they will turn to en bloc. And en bloc deals tend to be priced even more aggressively than GLS tenders because the selling owners are also negotiating their own exit price, not competing against a public floor.

The government's broader urban rejuvenation goal makes the policy shift internally consistent. Singapore is not getting any bigger. Existing land needs to be used more intensively, and aging developments need to be redeveloped to maintain housing supply. Fewer GLS sites plus easier en bloc thresholds equals the same outcome by different routes.

For buyers, this reinforces two things. First, average launch prices will keep climbing. Second, the resale market for aging freehold and older leasehold developments in prime en bloc corridors could see another wave of speculative bid-up, owners in the 70-80% support range will start acting like they are a year away from a payout, even before any deal is inked.

What this means for buyers right now

The 1H2026 slate is not a single headline. Several threads run through it, and they all point in the same direction.

If you are shopping for resale, the asking prices are real, but the transaction prices are negotiable. Average listings are inflated by owner ambition. The deals that close are the ones where buyers and sellers find the gap between asking and reasonable, and resale buyers who take the time to look at multiple units in the same development often find one priced 5-8% below the cluster. The slowdown you are reading about is actually a buyer's window if you are willing to be selective.

For new launch shoppers, start budgeting for 2027 floor prices, not 2025 floor prices. The Lentor Central $1,278 psf ppr bid in March 2026 is already reshaping OCR launch expectations. The Bukit Timah Road $1,820 psf ppr bid is already reshaping CCR. Every site that tenders in 1H2026 will set another reference number. By the time the 2027 launches arrive, anything priced below $2,800 psf in OCR or below $3,500 psf in CCR will feel like a win, not a premium.

If you are waiting for a GLS correction, we have not seen one in over a decade. Between 2014 and 2020, there were some softer tender periods, but even then, actual drops in land rates were modest and short-lived. Since 2021, every direction has been up. Betting against that trend requires a macro shock that is not visible in the near-term data. Interest rates are stable. Immigration policy is reinforcing demand. Construction costs are sticky. The conditions that would produce a meaningful correction are not in place.

On the holding period, remember that the Seller's Stamp Duty window is four years. That is the minimum hold period to avoid paying SSD on exit. Your discipline on holding through the SSD window matters more than your timing on entry, especially in a market where land costs keep rising. A unit bought well at 2026 prices, held through 2030, sits in a pricing environment shaped by whatever the 1H2026 and subsequent GLS programmes produce. That is the reference frame that matters.

The plot-by-plot read

Market commentary articles do not carry a single QPE rating, but we do flag per-plot reads when we have enough data to justify it. Based on what is public so far:

Bayshore Drive Integrated: strong on every fundamental except local demand depth, which the precinct-level transformation should solve over time. Top one or two plots in the slate on sheer quality. Preliminary read: 8.5-9 / 10.

New Upper Changi Road: deep HDB upgrader pool, mature estate, first major Bedok GLS in 15 years. The most plug-and-play "will sell fast at launch" plot on the list. Preliminary read: 9 / 10.

Berlayar Drive: strong on location and sea-fronting potential, but Greater Southern Waterfront demand builds over a longer horizon, not in a single launch weekend. For buyers who prioritise low-density waterfront living, this is the plot. Preliminary read: 7.5-8 / 10.

Peck Hay Road: CCR boutique play. Size constraints and the shadow of the $1,820 psf ppr Bukit Timah Road record mean pricing will be aggressive. Preliminary read: 6.5-7 / 10.

Holland Plain: pleasant, solid, but not distinctive. For buyers specifically anchored on the Holland Village precinct. Preliminary read: 6.5 / 10.

River Valley Green Parcel: crowded micro-market, limited view options, strong base location. Preliminary read: 6 / 10.

Lorong Puntong: boutique family play. Small site, strong school anchor, Thomson View launch timing will influence pricing dynamics. Preliminary read: 7 / 10.

Canberra Drive EC: routine estate-level addition. First-time HDB upgrader territory. Preliminary read: 6.5 / 10.

Sembawang Drive EC: furthest EC site, leans on the long-term Sembawang transformation case. Preliminary read: 5.5-6 / 10.

These are preliminary reads only. Actual tender results, winning developers, and eventual floor plans will reshape each number significantly. As tenders close and layouts become public through 2026, each of these plots will get its own full GLS analysis.

How to read the 1H2026 slate

Macro direction: Land costs are resetting the entire pipeline, 1H2026 GLS supply is down 10%, and the Bukit Timah Road $1,820 psf ppr record is already setting a CCR ceiling that the next tender will have to justify not exceeding. The structural case for continued price growth is built on four reinforcing trends: shrinking state land supply, rising developer bids, immigration-driven demand, and the potential relaxation of en bloc thresholds. None of those trends are pointing in the opposite direction.

Resale market: Slower than new launches, but not cheaper in any meaningful sense. Owners are asking all-time-high prices, and good units at reasonable asking prices still move. The opportunity is in selective buying, not in waiting for a broad price drop that is not coming.

1H2026 standouts: New Upper Changi Road and the Bayshore Drive integrated site are the two plots that will most likely define OCR launch benchmarks when they come to market in late 2027 or 2028. Berlayar Drive is the plot for low-density waterfront buyers. Peck Hay Road is the plot for CCR buyers who can stomach aggressive pricing. Everything else is supporting cast.

What to actually do: Pick the right property at the right price within your budget, and hold through the SSD window. That approach has beaten every timing strategy of the last decade, and nothing in the 1H2026 slate suggests the next few years will be different.

Data sources: URA GLS 1H2026 Programme, URA REALIS, EdgeProp, The Edge Singapore, 99.co, PropNex market reports, Huttons market commentary, Stacked Homes, Yahoo Finance Singapore

Published by MJ Review Homes (reviewhomes.sg) | PropNex Realty Pte Ltd | Shaik Amar R058640H | Myra Jalil R058979B | +65 9690 5440 | +65 9738 3705