HDB Resale Price Index fell 0.1% in Q1 2026 — the first quarterly decline since Q2 2019, ending a 22-quarter streak of uninterrupted growth. With 100,000+ BTO flats delivered since 2021, another 13,400 reaching MOP this year, and 8 in 10 HDB buyers fully CPF-financed, the conditions for a sustained correction are in place. The 2013-2020 downturn — which ran for nearly seven years under similar structural conditions — is the closest precedent. Older resale flats face the most exposure. Fresh MOP flats still hold a subsidy buffer. If you bought between 2021 and 2025 with heavy CPF, run your refund calculation now.

Sources: HDB, The Straits Times, CPF Board, data.gov.sg

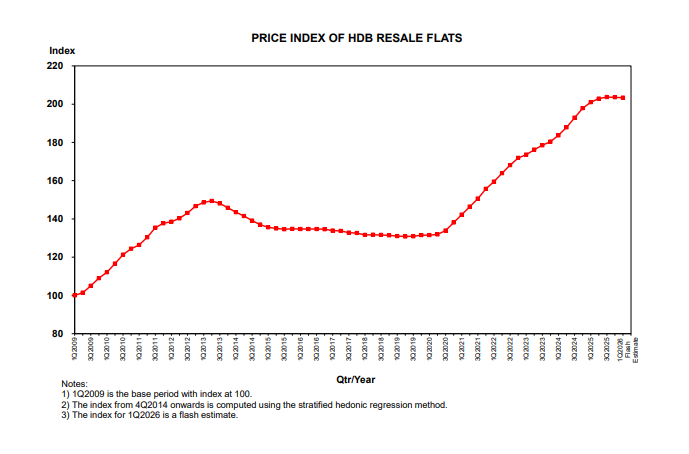

The streak is over

For 22 consecutive quarters, from Q2 2020 through Q4 2025, HDB resale prices went in one direction only. Up.

That run ended on April 1, 2026.

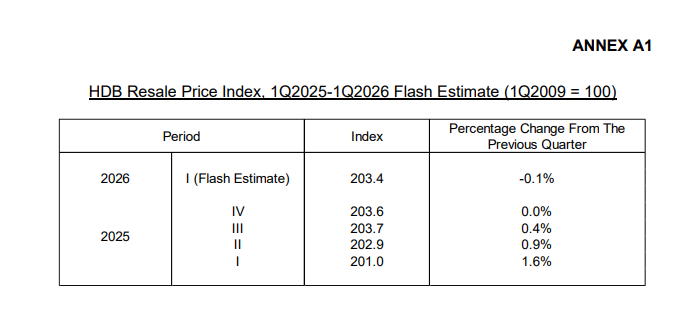

HDB's flash estimate for Q1 2026 shows the resale price index fell 0.1% quarter-on-quarter. A fraction of a percent. Barely a rounding error on any individual transaction. But it is the first quarterly decline since Q2 2019, close to seven years ago, and it lands after five straight quarters of decelerating growth.

Source: HDB

The trajectory tells the story more clearly than any single quarter:

| Quarter | QoQ Change | What Happened |

|---|---|---|

| Q1 2025 | +1.6% | Still rising, but slower than 2024 |

| Q2 2025 | +0.9% | Growth halved in one quarter |

| Q3 2025 | +0.4% | Barely moving |

| Q4 2025 | 0.0% | Flat — first time since Q1 2020 |

| Q1 2026 | -0.1% | First decline in nearly 7 years |

Source: HDB

Transaction volume confirms what the index is showing. There were 6,179 resale transactions in Q1 2026 (up to March 30), down 4.5% from the 6,473 recorded in the same period last year. Fewer buyers. Lower prices. The market appears to have turned.

Annual price growth already collapsed from 9.7% in 2024 to 2.9% in 2025. If Q1 2026 is any indication, 2026 could end flat, or negative for the full year.

100,000 BTOs: the cooling measure that actually worked

Three rounds of property cooling measures since 2020. ABSD hikes. Loan-to-value tightening. The 15-month wait-out period. All of these slowed demand at the margins, but none of them put a ceiling on HDB resale prices.

What did? Supply.

The government committed to launching 100,000 BTO flats from 2021 to 2025. They exceeded that target: 102,400 flats were launched across five years:

| Year | BTO Flats Launched |

|---|---|

| 2021 | 17,100 |

| 2022 | 23,200 |

| 2023 | 22,800 |

| 2024 | 19,600 |

| 2025 | 19,700 |

| Total | 102,400 |

And the pipeline is not slowing down. Another 25,000-plus flats are planned for 2026 and 2027, pushing the total from 2021 to 2027 to around 130,000 new HDB units. That is an enormous injection of supply into a market that was overheating precisely because there were not enough homes.

But the BTO supply does not only suppress demand for resale flats by giving buyers an alternative. It creates a second wave of supply pressure when those flats hit their Minimum Occupation Period.

In 2026 alone, an estimated 13,400 flats will reach MOP, nearly double the number in 2025. These are owners who can now sell on the open market, and many of them will, especially HDB upgraders looking to move into private property. That is 13,400 additional resale units entering the market on top of existing supply.

This was always the plan. The government said it publicly: make public housing affordable by building more of it. And after five years of relentless supply, it is working.

The CPF negative sale problem — and why it could get worse

Here is where it gets uncomfortable for a lot of Singaporean homeowners.

In 2023, close to 8 in 10 HDB buyers serviced their loans entirely with CPF contributions, little or no cash payments. The Housing Board published this statistic as a sign that housing is affordable. And from one angle, it is. A couple buying a four-room resale flat in Clementi for $750,000 can receive up to $80,000 under the CPF Housing Grant and another $20,000 from the Proximity Housing Grant. That is $100,000 in grants. Between that and their CPF Ordinary Account balances, many first-time buyers are covering their down payment, monthly mortgage, and everything else without touching their bank account. (Source: The Straits Times)

From 2020 to 2023, HDB handed out more than $4.5 billion in housing grants:

| Year | Grants Disbursed |

|---|---|

| 2020 | $1.02 billion |

| 2021 | $1.15 billion |

| 2022 | $1.13 billion |

| 2023 | $1.22 billion |

| Total | $4.52 billion |

Around 63,700 households received the Enhanced CPF Housing Grant (up to $80,000). Another 41,600 tapped the CPF Housing Grant. And 44,700 received the Proximity Housing Grant (up to $30,000). The system is doing what it is designed to do: helping Singaporeans buy homes.

But there is a catch that most first-time buyers do not think about until it is too late: CPF accrued interest.

When you withdraw CPF to pay for your flat, whether for the down payment or your monthly mortgage, the CPF Board tracks every dollar. And it charges you 2.5% interest per year on those withdrawals, compounded. This is the interest your CPF would have earned if it had stayed in your Ordinary Account. When you sell the flat, you have to refund the full amount: every dollar of CPF you used, plus all the accrued interest.

This is not a penalty. It is not a fee. It is a refund to your own retirement account. But it means that your "breakeven" on a flat sale is not just the purchase price. It is the purchase price, plus your outstanding loan, plus every cent of CPF used, plus years of 2.5% compound interest on top.

Here is what that looks like in practice. Note: since September 2022, HDB loan LTV was reduced from 80% to 75%. That means today's buyers put down 25% instead of 20%, more CPF upfront, more accrued interest from day one.

CPF Negative Sale: A Worked Example

Based on a $750,000 resale flat purchase, fully CPF-financed, HDB loan at 75% LTV (current rules)

| Purchase price | $750,000 |

| Grants received (CPF Housing + Proximity) | $100,000 |

| HDB loan (75% LTV) | $562,500 |

| Down payment from CPF (25%) | $187,500 |

| — of which $100,000 came from grants (credited to CPF OA first) | |

| Monthly mortgage from CPF (2.6%, 25yr) | ~$2,550/mth |

| CPF used for mortgage over 4 years | ~$122,400 |

| Total CPF withdrawn (down payment + mortgage) | ~$310,000 |

| Accrued interest (2.5% p.a., compounded) | ~$25,000 |

| Total CPF refund needed at sale | ~$335,000 |

| Outstanding loan after 4 years (reducing balance) | ~$495,000 |

| Total you owe at sale (loan + CPF refund) | ~$830,000 |

Sell at $750,000 (no change in price): Pay off loan ($495K). Remaining = $255,000. CPF refund needed = $335,000. Shortfall = $80,000. Negative sale. Zero cash.

Sell at $700,000 (6.7% drop): Pay off loan ($495K). Remaining = $205,000. CPF refund needed = $335,000. Shortfall = $130,000. Deeper negative sale.

To walk away with any cash at all, this flat needs to appreciate to at least $830,000 — a 10.7% gain — just to break even. Anything less and every dollar goes to the bank and CPF.

Read that again. Even if the flat sells at the exact same price you paid — $750,000 — you walk away with nothing. Zero cash. The entire sale goes to paying off the bank and refunding CPF.

Why? Because ~$55,000 of your monthly mortgage payments went to loan interest (money the bank keeps), and another $25,000 got added as CPF accrued interest. That is $80,000 in "invisible costs" that you never see but always owe. You need 10.7% appreciation over four years just to break even on cash.

And the longer you hold in a flat or declining market, the worse it gets, because CPF accrued interest keeps compounding at 2.5% every year regardless of what the market does.

Now multiply this across the hundreds of thousands of Singaporeans who bought resale flats between 2021 and 2025 at elevated prices, financed almost entirely with CPF. Many of them came in at the peak. Many of them are now watching prices flatten and start to dip.

We have seen this before: 2013 to 2020

This is not a hypothetical scenario. Singapore went through exactly this cycle once before — and it lasted seven years.

HDB resale prices peaked in Q3 2013. From there, prices declined quarter after quarter, all the way through to Q2 2019. For nearly seven years, the resale market moved in one direction: down.

During that period, CPF negative sales became widespread, particularly among owners of 3-room and 4-room flats purchased between 2011 and 2014 at peak prices. According to analysis by Stacked Homes, these buyers were the most at risk of walking away with zero cash when they sold. Older flats built before 1992 were especially vulnerable during the 2016-2020 stretch of the downturn. (Source: Stacked Homes)

The CPF Board's own rules acknowledge this happens: if your sale proceeds after paying off the outstanding loan are insufficient to cover the full CPF refund, you do not need to top up the shortfall in cash, provided you sold at or above market value. That policy exists because negative sales are not an edge case. They are a structural outcome when prices decline after a period of heavy CPF-financed purchases. (Source: CPF Board)

In practice, what happened was predictable. Sellers who needed to move, for an upgrade, a downgrade, divorce, financial pressure, had no incentive to hold out for a higher price. They were not going to see any cash regardless. Whether they sold at $500,000 or $480,000, the entire amount went to the bank and back to CPF. So they sold fast. And that pushed prices down further.

Buyers had endless options. Sellers got desperate. It was a buyer's market for seven straight years.

The parallels to where we are now are hard to ignore. The 2021-2025 buying cohort mirrors the 2011-2013 cohort: elevated prices, heavy CPF usage, and a government that has just spent five years flooding the market with new supply. The key difference is scale: more flats were sold at higher prices this time, and CPF financing rates are higher (8 in 10 now versus a lower proportion a decade ago).

The 15-month wait-out: will it stay?

One policy to watch closely is the 15-month wait-out period for private property owners who want to buy an HDB resale flat. Introduced in September 2022 as a cooling measure, it forces anyone who owns or has recently sold private property to wait 15 months before purchasing a resale flat.

In March 2026, the government addressed this in Parliament directly. The response: the policy is under active review, but "while the recent data looks promising, it is prudent to monitor for a while more before making any adjustments."

Reading between the lines, the government could reduce the waiting period gradually, perhaps from 15 months to 9 or 12 months first, rather than removing it entirely in one shot. A full removal could reopen the floodgates for private property downgraders entering the HDB resale market, and that risks pushing prices right back up. The government has spent five years engineering this correction. They are unlikely to undo it overnight.

Our guess is that if you are a private property owner waiting for the ban to lift so you can downgrade to HDB, expect to keep waiting through at least the rest of 2026. The government wants to see prices come down further before they ease up.

Who gets hurt, who benefits

Not all HDB owners face the same risk. Where you sit depends on when you bought, what you bought, and how you financed it.

Most exposed: resale flat buyers from 2021-2025 who financed fully with CPF. This is the group facing CPF negative sale risk within the next 3-5 years if prices continue to decline. The higher your purchase price and the more CPF you used, the faster accrued interest erodes your position. Older resale flats, 10 years and above from TOP, will feel the pressure first, because they have no subsidized-price advantage to fall back on.

Less exposed: BTO owners approaching MOP. If you bought a BTO between 2020 and 2022 and it is hitting MOP in 2025-2027, you bought at a subsidized price that is significantly below current resale values. Even in a declining market, you have a substantial built-in buffer. Million-dollar HDB transactions from fresh MOP flats are likely to continue: they are selling the government subsidy premium, and that premium is unlikely to evaporate just because the resale index dips 0.1%.

Benefiting: younger buyers looking to enter the resale market. This is what the government has been engineering. Affordable public housing means prices that come down to where first-time buyers can actually reach them without stretching beyond their means. If you are a young couple saving up for your first resale flat, 2026 and 2027 could offer better value than anything available since 2019.

What this means if you are buying or selling right now

If you are buying a resale flat: You have leverage for the first time in years. Transaction volume is falling, sellers are competing for fewer buyers, and the quarterly data is on your side. There is no rush. View more units. Negotiate harder.

If you have any intention of selling in the future, whether to upgrade to private, downsize, or relocate, seriously consider paying your monthly mortgage with cash instead of CPF. Yes, it means less cash in your pocket each month. But every dollar you pay from CPF gets tagged with 2.5% accrued interest that compounds silently for as long as you own the flat. Pay with cash and that accrued interest never starts. When you eventually sell, the difference between walking away with $80,000 in hand versus $0 could come down to this one decision.

This does not apply if you are buying a forever home. If you plan to live in this flat until the lease runs down and never sell, CPF financing is fine, accrued interest only matters at the point of sale. No sale, no refund, no problem. But be honest with yourself about whether "forever" really means forever. Life changes. Jobs change. Families grow. If there is even a chance you sell within 10-15 years, protect your cash position from day one.

If you are selling a resale flat: The window to get top dollar is almost closed. If you are sitting on a flat you bought pre-2020 with a healthy margin above your CPF refund, you are still in a strong position. But every quarter of decline eats into that margin. If you are planning to sell in the next 1-2 years anyway, for an upgrade, a downgrade, or any other reason, moving sooner rather than later gives you more cash in hand.

If you own private property and want to downgrade: The 15-month wait-out might not be going away this year. Plan accordingly. The silver lining is that when it eventually eases, you will be buying into a softer resale market. Patience works in your favour here, even if the wait is frustrating.

If you are waiting for a BTO: Keep waiting. Subsidized pricing plus the current market trajectory means your BTO purchase in 2026-2027 locks in a price that will look very reasonable within a few years. The government is unlikely to make BTOs more expensive: keeping public housing affordable for the next generation has consistently been a core priority.

Where we land on each thread

There is no single QPE rating for a market commentary. But here is where we land on each thread:

On the price decline: The 0.1% drop is a signal, not a crisis. It matters because it breaks a 22-quarter streak of uninterrupted growth. The direction has changed. Whether it accelerates into a sustained correction or flatlines for a few quarters before stabilizing depends on supply absorption, and with 13,400 MOP flats hitting the market this year plus continued BTO launches, supply pressure is not easing.

On BTO supply as a cooling measure: It worked. Three rounds of cooling measures slowed demand. But it was the 100,000+ BTOs that actually brought prices to a halt. The government now has proof that building aggressively is the most effective lever they have. We expect them to keep pulling it.

On CPF negative sales: This is the risk that most HDB owners are not thinking about yet. For the 80% of buyers who finance entirely with CPF, a sustained price decline of even 5-10% over the next few years could mean walking away from a sale with nothing. The 2013-2020 cycle proved this is not theoretical. It happened for seven years. The same structural conditions, peak prices, heavy CPF usage, and a supply-driven correction, are in place now.

On the 15-month wait-out: The government is likely to move cautiously. We expect a gradual reduction rather than a full removal, and probably not before late 2026 at the earliest. Lifting it entirely while prices are still fragile could reignite demand from private property downgraders, exactly the opposite of what they have been working toward.

For buyers: you are entering a market that favours patience. For sellers who bought between 2021 and 2025 at peak prices, the CPF refund calculation is the number to run right now, before the market runs it for you.

Data sources: HDB flash estimate Q1 2026, HDB press releases, CPF Board, The Straits Times, data.gov.sg, MND parliamentary Q&A March 2026

Published by MJ Review Homes (reviewhomes.sg) | PropNex Realty Pte Ltd | Shaik Amar R058640H | Myra Jalil R058979B | +65 9690 5440 | +65 9738 3705