We pulled HDB resale medians from data.gov.sg and condo resale prices from URA caveat data across three matched pairs: Bishan with District 20, Queenstown with District 3, Tampines with District 18. The 4-room HDB in each town grew 40 to 57 percent in 10 years. The 3-bedroom condo next door grew 71 to 80 percent. The price gap between the two doubled — from $436K-$628K in 2016 to $881K-$1.27M today. The Bishan pair went from $533K to $1.095M. Upgrading is twice the financial move it was a decade ago.

Sources: data.gov.sg HDB resale datasets, URA caveat data via squarefoot.com.sg

How much did the price gap widen?

Back in 2016, a 4-room HDB in Bishan was going for around $570K. A 3-bedroom resale condo in District 20, a few streets away, was going for around $1.103M — about $533K more. Today the same HDB sells for $795K and the same condo for $1.89M, putting the price gap at $1.095M.

Twice the gap for the same upgrade. We ran the numbers in three towns: Bishan, Queenstown, Tampines. The doubling showed up in all three.

The three matched pairs

We picked three towns where the HDB and the condo sit a few blocks apart, so the comparison isn't abstract:

- Bishan (HDB town) against District 20 (Bishan, Thomson, Ang Mo Kio condos)

- Queenstown (HDB town) against District 3 (Queenstown, Tiong Bahru, Bukit Merah condos)

- Tampines (HDB town) against District 18 (Tampines, Pasir Ris condos)

For each, we compared the 4-room HDB resale median from data.gov.sg against a 3-bedroom condo resale at typical size (1,050 sqft) in the matching district, using URA caveat data via squarefoot.com.sg. Full methodology at the bottom.

| Pair | 2016 HDB | 2016 condo | 2016 gap | 2025 HDB | 2025 condo | 2025 gap | Gap widening |

|---|---|---|---|---|---|---|---|

| Bishan ↔ D20 | $570K | $1,103K | $533K | $795K | $1,890K | $1,095K | +105% |

| Queenstown ↔ D3 | $685K | $1,313K | $628K | $988K | $2,258K | $1,270K | +102% |

| Tampines ↔ D18 | $425K | $861K | $436K | $668K | $1,549K | $881K | +102% |

All three pairs widened by roughly the same amount, give or take three percentage points. None held steady.

Why HDB grew slower than condo

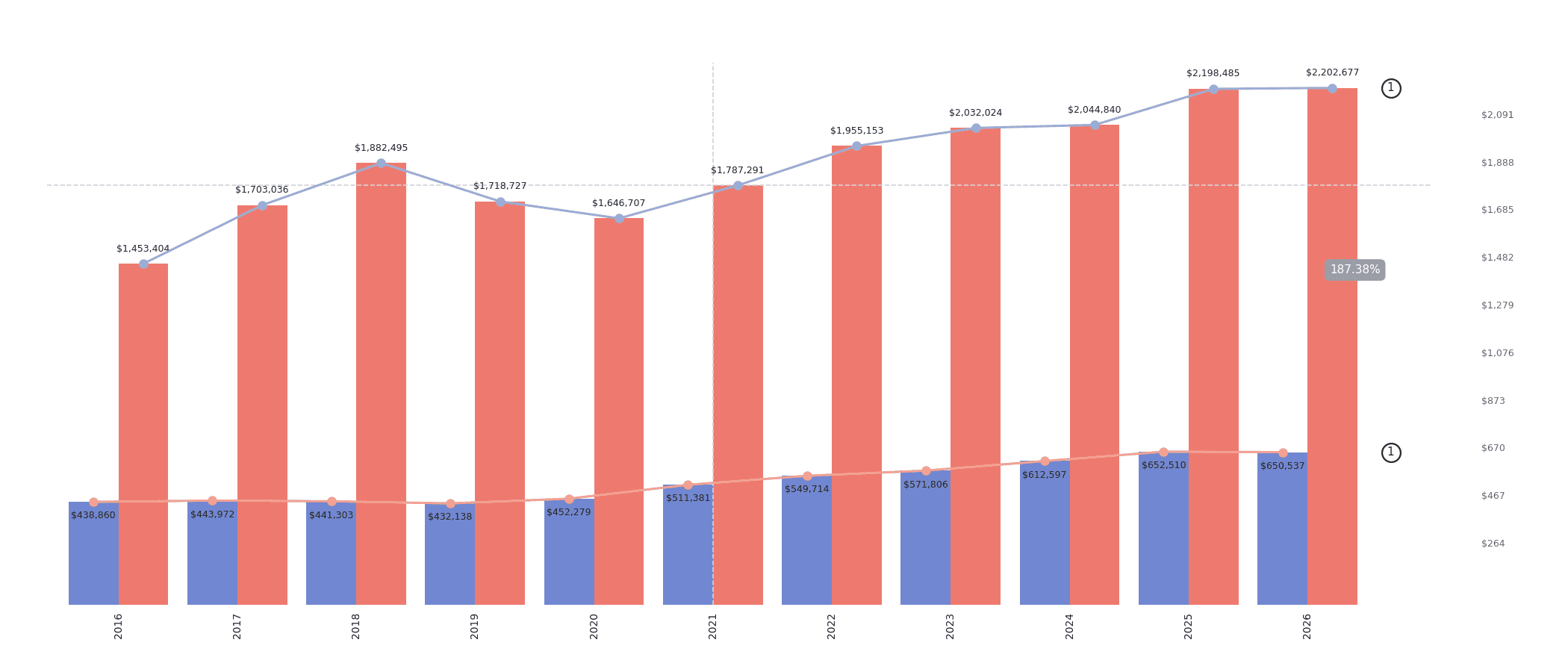

HDB 4-room prices in these towns grew 40 to 57 percent over the decade — not flat by any measure. Bishan moved from $570K to $795K. Queenstown crossed the million-dollar median. Tampines grew fastest at +57 percent.

Condo resale PSF in the same districts grew faster, 71 to 80 percent. District 20 went from about $1,050 PSF to $1,800. District 3 from $1,250 to $2,150. District 18 from $820 to $1,475. You can see the three trend lines below.

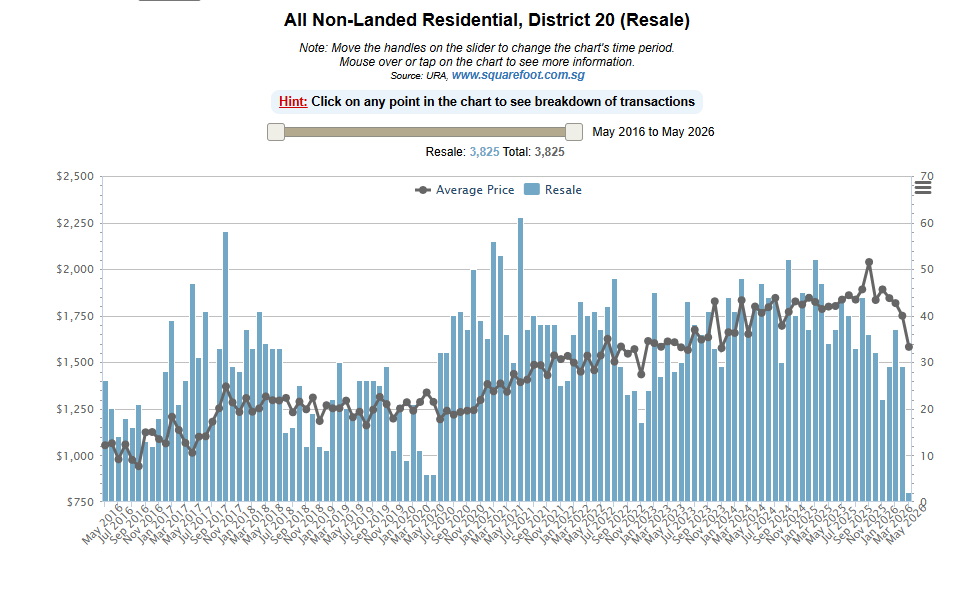

District 20 (Bishan / Thomson / Ang Mo Kio) — resale only. Source: URA caveat data via squarefoot.com.sg.

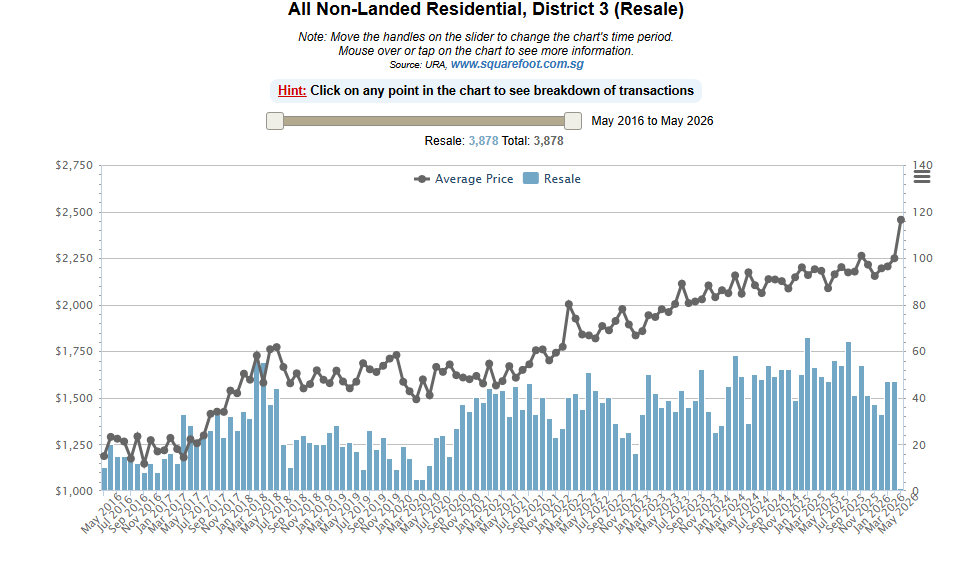

District 3 (Queenstown / Tiong Bahru / Bukit Merah) — resale only. Source: URA caveat data via squarefoot.com.sg.

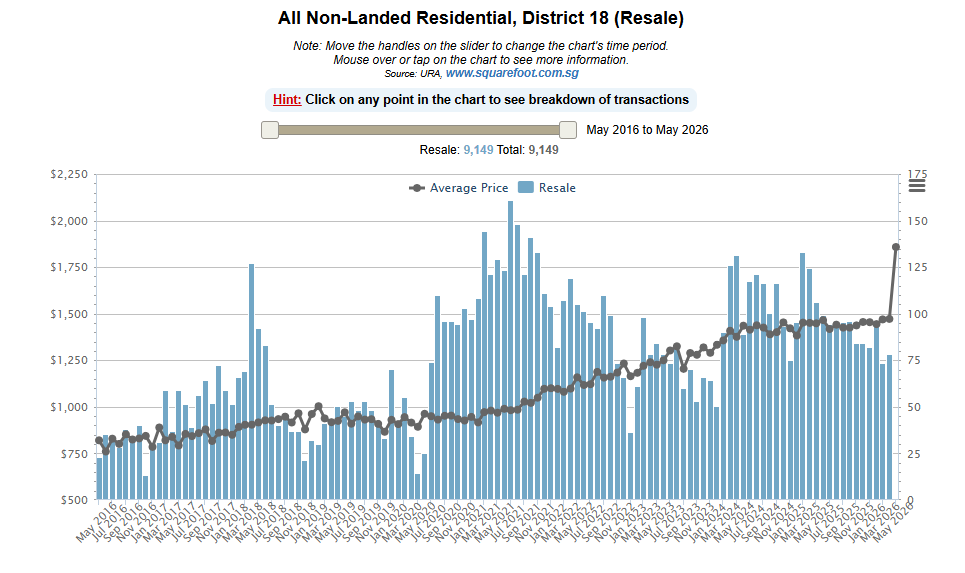

District 18 (Tampines / Pasir Ris) — resale only. Source: URA caveat data via squarefoot.com.sg.

There are three drivers behind the widening, and the largest agency in Singapore has flagged the same pattern. In April 2026, Wong Siew Ying, Head of Research and Content at PropNex, warned that "a widening HDB resale-private housing price gap over time may potentially make the leap for HDB upgraders more challenging." Her note went out the same week HDB resale prices booked their first quarterly decline in nearly seven years, while OCR private home prices rose 2.2 percent in the same quarter.

HDB has more supply. Wong attributes the cooling to it directly: from 2021 to 2025, HDB launched more than 102,000 new BTO flats, with another 25,000 lined up for 2026-2027. Each BTO clears its 5-year MOP and feeds back into resale. That keeps a lid on HDB prices.

Condo supply has not. New condos come from government land sales and en bloc deals, both of which slowed sharply after the 2018 cooling measures. 2024 was the lowest new-launch year in over a decade. With fewer condos coming out and the same buyers chasing them, prices push up.

The income side amplifies both. Top-decile Singapore household income has grown faster than the median over the past decade. More dual-income families crossed the $200K-plus mark, roughly what you need to service a $2M mortgage under TDSR 55. Those buyers keep showing up at private launches. HDB buyers, meanwhile, run into income ceilings on new flats and a thinner pool willing to pay close to a million for old resale.

That is how condo PSF runs about 1.7x ahead of HDB across the decade. And how the dollar gap doubles in ten years.

What does the doubled gap actually cost?

Percentages are easy to read. The cash takes longer to sink in.

A Bishan 4-room owner in 2016, selling at the $570K median and looking at a 3-bedroom resale condo in District 20, faced this stack:

- HDB sale proceeds after CPF refund and outstanding loan: roughly $300K-$400K cash, depending on how much CPF was used

- 3-bedroom condo at $1.103M: down payment 25 percent = $276K, of which 5 percent ($55K) must be cash

- BSD on $1.103M: about $32,000

- Legal, agent, valuation, renovation: $80K-$120K

- Loan: $828K (75 percent LTV), monthly mortgage around $3,300 at 2016 SORA rates (~1.8 percent)

For a couple earning around $200K combined, that upgrade was reachable.

The same owner in 2026, selling at $795K and looking at the same 3-bedroom in the same district at $1,890K:

- HDB sale proceeds: still in the $300K-$500K range depending on CPF

- 3-bedroom condo at $1.89M: down payment $473K, of which $95K must be cash

- BSD on $1.89M: about $63,000

- Legal, agent, valuation, renovation: $100K-$150K

- Loan: $1.418M (75 percent LTV), monthly mortgage around $4,960 at today's fixed-rate packages (~1.6 percent)

The down payment alone went up by $197K. BSD almost doubled. Monthly mortgage went up by about 50 percent even though rates are roughly flat to 2016, because the loan itself is 71 percent bigger. HDB equity grew over the decade, but nowhere near enough to absorb those new line items.

What this changes for the upgrader

Two things to keep in mind if you are sitting on a 4-room HDB and thinking about the next move.

Your HDB equity is not what your uncle's equity was. If your reference point is an uncle (or anyone close to you) who upgraded in 2016-2018, throw their numbers out. Their gap was half of yours, and not because they planned better. The gap moved.

The cheapest condo in your target area can be the most efficient way across — but not just any cheap condo. The cheapest unit only works if the condo itself wins on quality and exit (here's our framework). A low price in a tower with bad layouts, no facilities, or a thinning resale pool isn't a discount. It's a future problem. What you want is the most affordable unit in an area where the condo holds up: good land per unit, layouts a family actually wants to live in, and a steady pipeline of HDB upgraders who will want it from you when you eventually sell. That is the lowest hanging fruit, and there are not many of them. We have a full piece coming up that names the ones we like. Join our Telegram to know when it drops.

This is the problem. Your savings grow in a straight line. Property compounds on an increasing base. Every year you wait, the entry price rises, the gap widens, and the deposit you need grows with it. You are not standing still while you save. You are falling behind at the speed of compounding. The only way to close the gap is to own the appreciating asset, not save toward it. Past a certain point, a salary alone no longer catches up.

How did we measure this?

For the HDB side, we used the median 4-room resale price by town for full-year 2016 and full-year 2025, from data.gov.sg public records. Sample sizes ran from 162 to 892 transactions per town per year, well above any thin-sample threshold. Median, not average, to keep outliers from skewing the comparison.

For the condo side, we used the average resale PSF for all non-landed in each district from URA caveat data via squarefoot.com.sg, smoothed over a six-month rolling window around May 2016 and May 2026 to dampen new-launch spikes. We applied that PSF to a 1,050 sqft 3-bedroom unit, a realistic resale size for the districts examined.

A few things we did not control for. We did not separate freehold from leasehold (both districts have a mix). We did not segment by building age, which affects PSF inside any district. And we only ran this for the three matched pairs: D20, D3, and D18. Other districts and their HDB towns are not in this analysis. The 1,050 sqft assumption is a midpoint; older stock skews larger, newer skews smaller. Swap in 950 or 1,150 sqft and the dollar numbers shift 5-10 percent, but the gap-doubled finding still holds.

If you want this run for a specific town pair, or run with different size or tenure assumptions, send a request and we will run it.