On May 8, MND extended the EC MOP from 5 to 10 years, scrapped the deferred payment scheme, raised the first-timer quota from 70% to 90%, and stretched the first-timer priority period from 1 month to 2 years. Full privatisation moves from year 10 to year 15. The rules apply to every EC GLS site tendering on or after May 8 — Canberra Drive (May) and Sembawang Drive (June) are the first two plots affected. The $16,000 income ceiling stays unchanged. Median new EC prices rose 120% from $797 psf in 2015 to $1,754 psf in 2025.

Sources: MND, The Business Times, PropNex, Cushman & Wakefield, URA Realis

What just changed

This morning, May 8, 2026, National Development Minister Chee Hong Tat announced the most material reset to the executive condominium scheme in years. Speaking at the opening of the NUS Institute of Real Estate and Urban Studies Living Symposium, he laid out four changes that take effect immediately for every EC government land sale site with a tender closing date on or after today.

The headline change: the EC minimum occupation period is doubled. Buyers of new ECs will now wait 10 years before they can sell their unit, rent out the whole unit, or purchase another residential property. The previous MOP was 5 years, and that is the rule the entire EC market has operated under since the scheme launched in 1995.

Three other changes land alongside it. The deferred payment scheme is scrapped for new ECs. The first-timer quota goes from 70% to 90% of units. And the first-timer priority period stretches from 1 month to 2 years. Together, the four moves reshape almost every aspect of how ECs get sold, financed, and held.

The income ceiling stays at $16,000 a month, unchanged despite industry calls to lift it.

Two EC plots sit on the 1H2026 GLS calendar: Canberra Drive (tender in May) and Sembawang Drive (tender in June). Both fall under the new rules. Whoever wins those sites will be building the first two ECs under the new regime, and their land bids in the next eight weeks will be the first real test of how the policy is being priced in.

The four changes in detail

| Lever | Before May 8, 2026 | From May 8, 2026 |

|---|---|---|

| Minimum Occupation Period | 5 years | 10 years |

| Full privatisation (sell to anyone, including foreigners and corporates) | 10 years | 15 years |

| Deferred payment scheme | Allowed (20% upfront, 80% at TOP, 2-3% premium) | Scrapped |

| First-timer unit quota | 70% (first 1 month) | 90% (first 2 years) |

| First-timer priority period | 1 month from launch | 24 months from launch |

| Income ceiling | $16,000/month | $16,000/month (unchanged) |

1. The 10-year MOP

This is the change that matters most. Under the old 5-year MOP, an EC buyer who took possession at TOP could be selling on the open market within 5 years, rolling profits into a private condo, and starting the cycle again. That window is now twice as long.

Buyers will need to fulfil 10 years of occupation before they can rent out the entire unit, buy another residential property, or sell their EC to Singapore citizens and permanent residents. Full privatisation, when the unit can be sold to any buyer including foreigners and corporate entities, moves from year 10 to year 15.

For most first-time families, 10 years is just a long primary stay rather than a constraint. For people who were treating ECs as a 5-year hold-and-flip play, the calendar just changed dramatically.

2. Deferred payment scheme scrapped

Under the DPS, EC buyers paid 20% of the purchase price upfront, with the remaining 80% deferred until temporary occupation permit. The convenience came with a 2-3% premium baked into the EC unit price. The scheme let some buyers reach into larger units than progressive payment math would have allowed.

That is gone for new ECs. The normal progressive payment scheme, where buyers pay milestones tied to construction stages, is now the only path available, the same as for other uncompleted private residential properties. MND framed the change as encouraging financial prudence and aligning EC payment treatment with the rest of the new launch market.

The practical effect: some buyers who would have stretched into a 4-bedroom EC under DPS will now sit at a 3-bedroom budget under standard progressive payment. That nudges aggregate demand toward smaller unit types and forces more upfront cash discipline.

3. First-timer quota lifted to 90%

This one rewrites the launch-day arithmetic. Currently, 70% of EC units are reserved for first-time home buyers during the first month of launch. After that month, developers can sell to any eligible buyer, including second-timers. The new rule lifts the reserved quota to 90% of units.

The data behind the change is telling. In 2020, about half of EC buyers were first-timers. By 2024 and 2025, the first-timer share had dropped to between 30% and 40% of buyers. Second-timers, typically families upgrading from an HDB flat with sale proceeds in hand, were progressively crowding out first-time families in the original target buyer pool.

A 90% first-timer reservation does not guarantee that 90% of buyers will be first-timers. It guarantees they get first call on 90% of units. But the combination with the next change is what really shifts behaviour.

4. First-timer priority period stretched to 2 years

Under the old rule, the 70% first-timer reservation lasted 1 month. After that, second-timers could mop up unsold inventory quickly, and historically they did. The new rule extends the first-timer priority period to 2 years.

This is the move likeliest to slow launch sales. Inventory unsold during a 1-month window typically clears fast in the second-timer phase. A 24-month priority period means developers are looking at roughly two years of slower absorption before second-timers can buy in volume. Combined with the 39-month window before the developer additional buyer's stamp duty clawback risk kicks in (or up to 60 months under prevailing remission timeline extensions, per Minister Chee's wording), the effective sales runway is much tighter than it looks.

This is the lever MND specifically called out as expected to drag on developer bidding behaviour. Developers do not pay the same psf for land they have to clear under a 24-month first-timer-only constraint as they would for a site they could clear in 12 months across all eligible buyers.

Why MND pulled this lever

Two trends pushed the policy review past the tipping point. The first is price. The second is flipping.

EC prices have outpaced OCR private

EC prices are no longer the affordable public-private hybrid the scheme was designed around. PropNex data shows median new EC prices rose from $797 psf in 2015 to $1,754 psf in 2025, a 120% increase over a decade. Over the same period, new OCR 99-year non-landed private homes rose from $1,150 psf to $2,252 psf, a 96% increase.

| Year | Median New EC psf | Median New OCR Private psf | EC discount to OCR |

|---|---|---|---|

| 2015 | $797 | $1,150 | 31% |

| 2025 | $1,754 | $2,252 | 22% |

| 2026 (as at Apr 26) | $1,843 | $2,278 | 19% |

The EC discount versus comparable private OCR homes has narrowed from 31% in 2015 to 19% by April 2026. The scheme's original design intent, a meaningful 20-30% pricing gap below private condos to compensate for the eligibility and ownership restrictions, is being eroded from the EC side, not the private side.

The Rivelle Tampines launch six weeks ago crystallised the concern. Rivelle moved 93% of its 572 units at an average of $1,893 psf, with three-bedrooms starting just under $1.6 million and the largest five-bedders going over $2.5 million. Those are private-condo-adjacent prices on a unit type that still carries an HDB-style income cap and resale restrictions.

Resale flipping hit record pace

The second pressure was the secondary market. About 75% of ECs sold on the open market between 2021 and 2025 transacted within 5 years of MOP, meaning owners were exiting almost as soon as they hit the eligibility window. The same figure for the 2016-2020 period was 45%. The flipping intensity nearly doubled in a decade.

Cushman & Wakefield data crunched for The Business Times shows ECs have topped the percentage-gain charts every quarter since Q1 2023. In Q1 2026, the top five most profitable EC resale deals recorded gross gains of 130% to 140%. Sellers walked away with over $1 million on units they bought as subsidised public-private hybrids a few years earlier. In Q1 2023, the equivalent top five gains sat at 83% to 86%.

The pattern is clean: buyer takes EC at subsidised land cost, holds 5 years to clear MOP, sells to upgrade-track buyers at private-adjacent prices, books the gap. Repeat across thousands of units a year, and the EC scheme stops looking like a housing programme and starts looking like a subsidised flip vehicle.

Land bids were already climbing

Developer land bids confirmed the same pattern. The two Woodlands EC plots that closed across August 2025 and January 2026 set fresh records: $782 psf ppr (CDL) and $794 psf ppr (Sim Lian). Those are land prices that almost guarantee EC launch psf above $1,800. Without an MOP extension and the DPS scrapped, those launches would have rolled out at numbers that further closed the EC-to-private discount.

MND has now pulled three levers to push back: longer MOP slows the flip cycle, scrapped DPS removes a financing stretch, larger first-timer quota with longer priority window forces developers to sell into a more constrained buyer pool. Cooler land bids are the intended consequence.

Who wins, who loses

Not every EC participant is affected the same way. The reset cleanly reshuffles who benefits and who loses access.

First-time buyers: biggest winners

Anyone who has not previously owned a property is the clear beneficiary. The 90% reserved quota plus 2-year priority period materially improves the odds of getting a unit at any new EC launch. The pool you are competing against shrinks dramatically. Second-timers cannot bid against you for the first 24 months. The 10-year MOP is largely irrelevant if you actually want to live in the unit for the medium term, which is the original scheme intent.

If your household income is under $16,000 a month, you are buying your first home, and you can hold for the long stretch, this is the most accessible EC environment in years. The Canberra Drive and Sembawang Drive launches will be the first to test it.

Second-timers: biggest losers

Anyone selling an HDB to upgrade into an EC is now competing for a much smaller residual unit pool. Under the old rules, you waited 1 month after launch and then had a clear runway to buy. Under the new rules, you wait 24 months. By then, the most desirable stacks and floors are gone, and the development is well past launch momentum.

For some second-timer families, the practical answer becomes: skip ECs entirely and look at OCR mass-market private condos. The pricing gap has narrowed to 19%, and a private OCR launch carries no MOP restriction, no income ceiling, and no eligibility paperwork. The EC value proposition for second-timers was already thinner than most buyers assumed. The new rules thin it further.

Existing EC owners: unaffected

If you bought an EC under the existing 5-year MOP framework, your unit continues to operate under the rules in force at the time of your project's tender award. Your 5-year MOP still applies. Your project still privatises at the 10-year mark. Your sale rights and rental rights to existing EC stock are not retroactively touched.

Resale liquidity for existing ECs may even tighten in the short term, because the supply of new ECs over the next 4-5 years will reach the open market under more restrictive flip conditions. That could put modest upward pressure on resale ECs that already cleared MOP. The data on this will come slowly, but the directional logic favours holders of existing post-MOP ECs.

Developers: pricing pressure both ways

Developers face a trickier sales window. The 24-month first-timer-only phase compresses absorption. The 39-month sales window before ABSD clawback risk shrinks effectively. The 90% quota means they cannot lean on second-timer demand for two years. All three push toward more conservative land bids.

Whether developers actually moderate bids at Canberra Drive and Sembawang Drive will tell us how the policy is being internalised. The announcement landed today; the Canberra Drive tender closes within weeks. If land prices for the May and June plots come in materially below the $782-$794 psf ppr Woodlands references, the policy is working as intended. If they hold or set new highs anyway, MND has more work to do.

Private new launch and resale: where displaced HDB upgraders go

Our read is that the bulk of HDB upgraders priced out of the EC second-timer queue will redirect to private new launches and resale, not wait 24 months for residual EC inventory. The arithmetic from the upgrader's seat is straightforward. With first-timers now reserved 90% of units across a 24-month priority window, the residual EC pool that opens up to second-timers is much thinner than the old 30%-after-one-month residual. By the time the priority period clears, the launch is two years old, the desirable stacks are gone, and the project is mid-construction. The 19% pricing gap to OCR private is real but narrow, and a private launch carries no MOP, no income ceiling, and no eligibility paperwork. Resale gives an upgrader immediate possession with no construction wait at all. Expect this redirect to show up in OCR launch absorption rates and in resale transaction volume across HDB-adjacent estates over the next 18-24 months.

Canberra Drive and Sembawang Drive: the first two tests

The 1H2026 Confirmed List carries two EC plots, and both fall squarely under the new rules. They will be the first to price the regime change.

Canberra Drive (EC): May tender

Approximately 1.14 hectares, an estimated 185 units, sitting behind Brownstone and Visionaire near Canberra MRT. The tender closes in May. Under the previous regime, the expected land rate would have sat in the $650-$680 psf ppr range that recent EC bids had been trending around. Under the new rules, the question is whether bids hold or pull back. A bid below $650 psf ppr would be a concrete signal that developers have adjusted their bids for the longer MOP and tighter sales window. A bid at or above the previous Woodlands records would suggest the cooling measures are not yet biting.

Sembawang Drive (EC): June tender

Approximately 450 units, the larger of the two plots, sitting further out from core amenities. The tender closes in June. Sembawang sits in a different demand pool than Canberra. It leans on long-term Sembawang shipyard area transformation, with thinner immediate amenity backing. Under the new rules, this plot is the more sensitive of the two to land-bid moderation. Developers pricing a 24-month first-timer-only window for an outer-OCR EC site should bid notably below where they would have under the old framework.

Both plots are now natural experiments. By end of June, we will have two data points on how the new EC rules translate into actual land prices. Those land prices will, in turn, set the baseline for whatever launches in late 2027 or early 2028.

What this means if you are buying or selling right now

If you are a first-time buyer eyeing an EC, your odds just improved materially. The 90% quota plus 2-year priority window is the most first-timer-friendly EC environment since the early days of the scheme. Get your eligibility paperwork in order. Run your mortgage affordability under standard progressive payment, since the DPS option is no longer there to stretch your budget. If your household sits comfortably under the $16,000 ceiling and you intend to live in the unit for at least a decade, the next two GLS launches are worth tracking closely.

If you are a second-timer hoping to upgrade into an EC, reset expectations. You are now waiting 24 months for the priority period to clear, and the 90% reserved quota means the remaining inventory will be picked over by the time you can buy. For many second-timer families, the cleaner option is to compare an OCR private launch directly against an EC. The 19% pricing gap is real but narrow, and you skip every restriction in the EC framework. Run both options side by side rather than defaulting to the EC route.

If you already own an EC under the old MOP, nothing changes for you. Your 5-year MOP, your 10-year privatisation timeline, your sale and rental rights all continue under the framework that applied at your project's tender award. If anything, the supply tightening on new ECs over the next 4-5 years could mildly support resale demand for existing post-MOP units. Hold and watch is fine. There is no need to rush a sale or change strategy.

If you were planning to flip an EC at MOP, that approach is largely dead for any future-tendered EC. A 10-year MOP with no purchase of another residential property in the interim removes the upgrade cycle that made fast-flipping work. Owners of pre-May-8 EC GLS projects can still execute their original plan, but anyone buying into a Canberra Drive or Sembawang Drive launch should price the unit on owner-occupation merit, not flip economics.

If you are a developer or watching land bids, the next two EC tenders are the cleanest read on how aggressively the new rules are being internalised. If the May Canberra Drive bid comes in well below recent Woodlands records, the policy is working as MND intended. If the June Sembawang Drive bid follows suit, the EC pricing trajectory has been reset for the next 3-5 years of supply.

What MND just reset

The 10-year MOP and the scrapped DPS are the substantive moves. Together they remove the two biggest drivers of EC flipping: fast resale eligibility and stretched financing. The 90% first-timer quota with 2-year priority is the structural fix. It rebuilds the original 1995 intent of the scheme: ECs as a step into private home ownership for first-time families, not a short-cycle investment vehicle for second-timers.

Whether the price-cooling effect actually materialises depends on how developers respond to Canberra Drive in May and Sembawang Drive in June. The framework is now in place. The execution will play out at those two tenders, and through whatever launches in 2027 and 2028.

For first-time buyers, this is the most welcoming EC environment in over a decade. For second-timers, who are mostly HDB upgraders sitting on sale proceeds, the EC route is materially less attractive. We expect most to redirect to private new launches and resale rather than wait 24 months for residual EC inventory, and the OCR private comparison deserves a fresh look. For existing EC owners, nothing changes. For the broader market, expect EC land bids to moderate, EC launch psf to soften by 2027, and the EC discount versus OCR private to widen back toward the 25-30% range the scheme was originally designed around.

The income ceiling staying at $16,000 is the one missing piece. With Rivelle Tampines launching at an average $1,893 psf and three-bedders starting at $1.6 million, the qualifying buyer pool was already being squeezed by affordability. MND has signalled the income ceiling is under review separately. If it does move up later this year, it would complete the recalibration. As of today, the four levers announced are doing the heavy lifting.

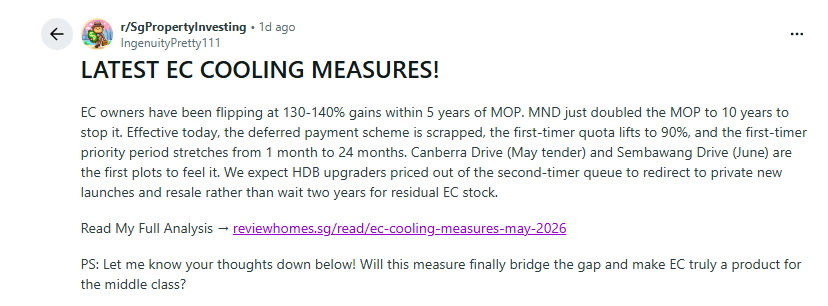

How Singaporeans are reading the cooling measures

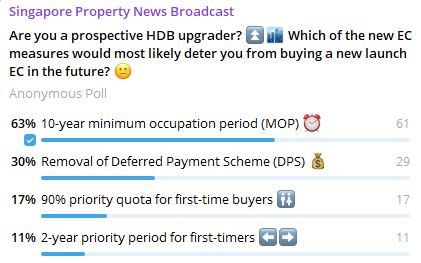

We posted our analysis to r/SgPropertyInvesting the day the rules dropped, and Singapore Property News Broadcast ran a poll asking prospective HDB upgraders which lever bites hardest. Here is what came back.

Before the Reddit comments, here is the broader sentiment from the Singapore Property News Broadcast poll. Close to 100 prospective HDB upgraders weighed in.

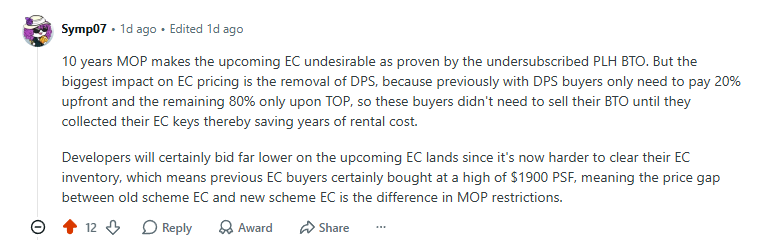

The poll's headline number: 63% of prospective HDB upgraders said the 10-year MOP is the biggest deterrent to buying a new launch EC. Removal of the DPS came second at 30%. The first-timer quota and priority window are minor concerns at 17% and 11% respectively. Read another way: among upgraders, the lifestyle constraint is what bites. They have the cash. They do not have a decade.

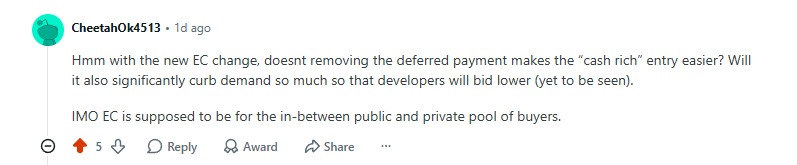

The Reddit thread came in with a different angle, weighted toward the DPS scrap as the bigger pricing lever and the long-cycle question of where the EC scheme lands if developers chase FOMO instead of adjusting prices down.

You can read the full thread on r/SgPropertyInvesting.

We read every reply. If there is a topic you want us to cover, a condo you would like reviewed, or a property journey worth telling — your own purchase, your near-miss, or what you are holding right now and trying to decide what to do with — write to us. Some of these become full articles on the site. Some become case studies. We have turned reader questions into full guides before, and we will do it again.

Send us a topic on WhatsAppData sources: MND announcement May 8, 2026 (Minister Chee Hong Tat at NUS IRES Living Symposium 2026), The Business Times reporting by Chong Xin Wei, PropNex median price data, Cushman & Wakefield resale gain data, URA Realis land bid data

Published by MJ Review Homes (reviewhomes.sg) | PropNex Realty Pte Ltd | Shaik Amar R058640H | Myra Jalil R058979B | +65 9690 5440 | +65 9738 3705