Thomson Reserve — the official launch name for the former Thomson View en bloc site — is the 1,240-unit Upper Thomson new launch by UOL, SingLand and CapitaLand, coming in Q3 2026 after the High Court cleared the $810 million collective sale on 1 July 2025. That deal remains the largest residential en bloc since Chuan Park. Land cost works out to $1,178 psf ppr, within 2% of Penrith's tender at Margaret Drive. Our preview QPE score is 8/10, with Quality and Exit strong and the Price pillar held until the developers release their numbers.

Thomson Reserve review: the $810M Thomson View en bloc now has a name

The condo that property buyers have been calling "Thomson View" for the last 18 months finally has its official launch name: Thomson Reserve. Same site, same plot, same UOL-SingLand-CapitaLand consortium, just a different name on the marketing materials. Every reference to Thomson View you see in this review applies to Thomson Reserve.

This is our original en-bloc preview. For the current read, go to our continuously updated Thomson Reserve review. It carries the published site plan and our live 8/10 call as the launch develops; this page stays as the en-bloc backstory.

Thomson Reserve has been Singapore's most anticipated launch since the land was awarded. It has also been one of the most delayed. The $810 million collective sale, the largest residential en bloc transaction since Chuan Park cleared at $890 million in May 2023, spent months tied up in the Strata Titles Board before the High Court finally approved it on 1 July 2025.

Now, with the ownership transfer done and the project name confirmed, Thomson Reserve is scheduled to launch in the second half of 2026. September or later is the operative window. After a year of rumours about whether the launch would hit Q2 2026, slip to Q3, or even get pushed into 2027, the developer guidance has settled on 2H 2026 with a showflat preview expected shortly before the sales launch.

This is a preview article. Floor plans are not out. Starting prices are not out. Unit mix ratios are not out. What is already locked in is the land, the developers, the location, the name, and the launch window. That is enough to build the QPE skeleton on Quality and Exit. Price is the one pillar we cannot rate until the developers release their numbers.

How we review: the QPE framework

Every review on this site runs through our QPE framework: Quality, Exit, Price.

Quality covers developer track record, land size, layouts, MRT access, views, and facilities. Exit asks who buys from you when it is time to sell, what the demand pool looks like, and what competing supply exists at resale. Price examines total price (not psf) and how it compares against what the market has tested. Is there a price gap, or are you paying above where the market has cleared?

All three need to check out. If one fails, you need to know which one, and why.

The Thomson View en bloc: how the deal finally closed (and became Thomson Reserve)

The collective sale set the developer's cost base and the launch timeline. Both feed directly into launch pricing.

The original Thomson View Condominium was a 254-unit 99-year leasehold from 1987 on 7-17 Bright Hill Drive, on 46,852 sqm at plot ratio 2.1. Owners first set a $918M reserve that could not clear the 80% mandate. At least 80% of the 206 owners eventually lowered to $808M, which cleared the way for the UOL-SingLand-CapitaLand $810M offer.

The developers exercised in November 2024. In March 2025, the Strata Titles Board issued a stop order after minority owners objected. The High Court approved the sale on 1 July 2025, with the transfer completed shortly after. Individual owners received between $2.22M and $4.94M depending on unit size.

The quiet headline: $810M came in 12% below the $918M original reserve. The developers got a discount, and that discount flows directly into the launch price.

The developers: UOL, SingLand and CapitaLand together

The consortium behind Thomson Reserve is the closest thing Singapore has to a maximum-strength delivery vehicle on a large residential site.

UOL Group brings the design discipline that delivered Watten House, Meyer House, The Tre Ver, and AMO Residences: consistent on launch day, sensible on price, no recent disasters. Singapore Land, a UOL subsidiary, carries the finishing-quality reputation built on Liv@MB in D15 and Pinetree Hill at Pine Grove. CapitaLand Development supplies the deepest balance sheet of the three, with One Pearl Bank's refurb-to-residential and the Sengkang Grand Residences JV on its recent record.

On a 1,240-unit site at this land cost, that consortium is the best any buyer could hope for. The variable to watch when the floor plans drop is common-room sizing; at this density, it is where project economics tend to compress first.

The land: 504,000 sqft of elevated ground

Source: OneMap (plot outline overlay)

Source: OneMap (plot outline overlay)

At 504,314 sqft, Thomson Reserve is one of the largest single residential plots to come to market in D20 in a decade. The plot runs elongated from the Bright Hill Drive frontage to the back, sitting elevated relative to the landed enclaves and the reservoir edge.

The orientation works in buyers' favour. Most residential units are expected to face south-southeast, which avoids the western sun and opens reservoir and landed views from the upper floors. Landed rooftops should be visible from floor 5 or 6; reservoir views from floor 10 and up.

Walk time is the trade-off baked into the elongated plot. The closest stacks to Upper Thomson MRT are under a minute on a covered walk. The far-end stacks add another six to eight minutes. Stack selection will matter as much as floor level, and the developer's stack premiums should reflect that.

Planning parameters: around 1,240 units across roughly seven towers at 24 storeys, plot ratio 2.1. That works out to 850 sqft of land per unit, which leaves substantial room for facilities. Expect multiple pools, a full tennis court, kids zone, and a 50m lap pool. None confirmed until the site plan drops.

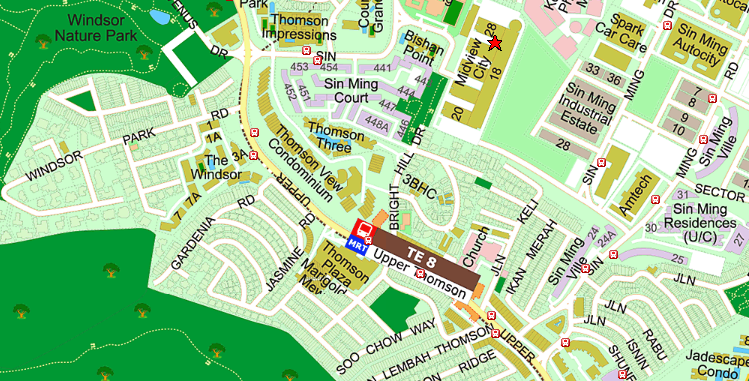

Thomson Reserve location: three TEL stations within walking distance

Transit

The closest stacks sit a one-minute sheltered walk from Upper Thomson MRT (TE8), which connects to Orchard in roughly 10 minutes and Marina Bay in 17 on the TEL. The line is one of the most productive in Singapore for rental demand and feeds directly into Exit.

Bright Hill MRT (TE7), also on the TEL, is walkable from the far-end stacks; some back-stack buyers will find Bright Hill the shorter walk. Marymount MRT on the Circle Line is a longer walk or a short bus ride and adds CCL orbital access plus the future CRL interchange. Two TEL stations walkable from the same condo is uncommon in Singapore.

Schools and amenities

Ai Tong School sits inside the 1km priority zone and will be a decisive draw for 3BR/4BR buyers at launch. Catholic High, Marymount Convent, and Kuo Chuan Presbyterian fall in the wider 1-2km radius. For upgrader families with primary-school-age kids, Ai Tong is the decisive draw.

The day-to-day amenity is Thomson Plaza, a neighbourhood mall linked to Upper Thomson MRT via an overhead bridge and an underground walk: supermarket, food court, cinema, services. Bishan Junction 8 is two MRT stops away for bigger runs. The Shunfu and Soo Chow Garden food row (Mingfa Fishball Noodles, the roti prata house, Soi 90 Thai, the salted caramel place) sits within ten minutes on foot. MacRitchie Reservoir and the TreeTop Walk are walkable via the second site entrance, which tends to show up meaningfully in resale demand.

Driving

CTE access is four to five minutes via Lornie Road. PIE is similar. SLE is slightly further. Central-north expressway access is convenient.

The traffic caveat is Upper Thomson Road outside Thomson Plaza, which jams from 6 to 8pm on weekdays as the mall carpark, school dismissal, and dinner rush stack on the same stretch. If you drive home during peak, factor it in. MRT riders are unaffected; the station sits below the jam.

Thomson Reserve price: what the land cost implies before launch

A caveat first: everything in this section is a pre-launch estimate, not a rating. We hold the Price pillar until the official price list is out — our live Thomson Reserve review puts our 3-bedroom price prediction on the record so you can hold us to it when the guide price drops. The build-up below shows where the land cost points, nothing more.

The starting prices have not been released. The land cost has. $810 million on a 504,000 sqft site with a plot ratio of 2.1 works out to $1,178 psf ppr.

Standard development margins in Singapore move that number from raw land cost to launch PSF through three layers: development costs (construction, fees, financing, marketing), harmonized adjustments (post-2023 regulatory changes to how unit sizes are calculated), and developer profit margin.

Working from $1,178 psf land cost:

- Land cost: $1,178 psf → +72% development costs → $2,026 psf → +8% harmonized adjustment → $2,191 psf → +20% developer margin → $2,627 psf

Baseline launch PSF is around $2,627 psf. Developers can price above or below based on how aggressively they price for velocity and how much market headroom they see.

Plausible launch range: $2,500 to $2,900 psf. Lower end is aggressive pricing for velocity (Penrith started 2BR at $2,437 psf in October 2025). Upper end is premium positioning that relies on developer brand and the MRT doorstep premium. Beyond $2,900 psf starts compressing the buyer pool that makes this a blockbuster.

Total prices by unit size:

| Unit Type | Est. Size (sqft) | At $2,500 psf | At $2,627 psf (baseline) | At $2,900 psf |

|---|---|---|---|---|

| 1BR | 484 | $1.21M | $1.27M | $1.40M |

| 2BR | 700 | $1.75M | $1.84M | $2.03M |

| 3BR compact | 900 | $2.25M | $2.36M | $2.61M |

| 3BR standard | 1,000 | $2.50M | $2.63M | $2.90M |

| 4BR | 1,300 | $3.25M | $3.42M | $3.77M |

| 5BR | 1,700 | $4.25M | $4.47M | $4.93M |

Unit sizes are estimates based on typical post-2023 harmonized floor plans at this price tier. Total price is what matters; PSF is secondary context.

The 3-bedroom is the price-sensitive segment. A 1,000 sqft 3BR at $2.63M (baseline) sits inside the normal HDB upgrader band with both incomes decent. At $2.90M, the upgrader pool compresses and demand leans on landed downgraders. At $3M+, it compresses further. This is the tier to watch when the developers release pricing.

Thomson Reserve vs Penrith: the closest reference point

Penrith at Margaret Drive is the closest launched reference for Thomson Reserve's land cost. Not because the locations are comparable (Penrith is D3 Queenstown, Thomson Reserve is D20 Upper Thomson) but because the GLS tender prices are within touching distance.

| Metric | Thomson Reserve (Thomson View site) | Penrith |

|---|---|---|

| Land cost | $1,178 psf ppr (en bloc, 2024) | $1,154 psf ppr (GLS, 2024) |

| Total units | around 1,240 | 462 |

| Tenure | 99-year leasehold | 99-year leasehold |

| MRT | Upper Thomson (TEL) | Queenstown (EWL) |

| Developers | UOL, SingLand, CapitaLand | Hong Leong, GuocoLand, Intrepid |

| Launch | 2H 2026 (expected) | October 2025 (done) |

| Starting PSF | TBD | $2,437 (2BR) |

| Average achieved PSF | TBD | around $2,800 |

| Launch-day take-up | TBD | 97% |

Penrith's land cost sits $24 psf ppr below Thomson Reserve, a 2% difference and negligible per unit. What matters: at lower land cost, Penrith still started 2BR at $2,437 psf and averaged $2,800 psf across launch day.

If Thomson Reserve tracks that pattern, starting PSF should land around $2,450-$2,500, average across all units around $2,700-$2,850. Consistent with the $2,627 baseline.

Scale differs: Penrith is 462 units, Thomson Reserve is 1,240. Larger launches tend to price starting units more aggressively to protect velocity, then push premium stacks up as absorption builds. Expect 1BR and compact 2BR at the lower end of the range, 4BR and 5BR at the upper end.

Thomson Reserve vs Upper Thomson resale: what already exists

The existing resale benchmark in the immediate micro-market is Thomson Impressions, a 288-unit 99-year leasehold development at Sin Ming Walk that TOP'd in 2019. Over the last 12 months, Thomson Impressions transactions have ranged from approximately $1,793 psf to $2,342 psf, with a median around $1,810 psf.

This is not a direct apples-to-apples comparison. Thomson Impressions is a smaller, older, different-developer product on a different plot. But it is the best available read on what buyers are currently paying for a private condo in this part of Upper Thomson.

The gap between Thomson Impressions resale (around $1,800 psf median) and Thomson Reserve's expected launch (around $2,500-$2,800 psf) is 35-55%. That premium pays for brand-new product, a larger plot, three top-tier developers, the scarcity premium of an en bloc this size, and a corridor that has not had a mega-launch this scale in over a decade. Defensible but not unlimited; the floor plans and Exit pool will show how much of that premium the resale market keeps.

What we do not know yet

Floor plans and unit mix are the biggest unknowns. Without them, room sizes, layout types, and efficiency ratios cannot be assessed. At 1,240 units, developers are tempted to compress sqft aggressively, so common-room sizes are the first thing to check when plans drop.

The facade and facilities are also unconfirmed. Expect premium contemporary cladding, a 50m lap pool, a full tennis court, kids zone, and clubhouse. None of that is locked in until the marketing materials release.

Unit mix ratios are not public yet either. Typical for a condo this size would be roughly 30% 1BR and 2BR, 50% 3BR, and 20% 4BR and 5BR. The actual mix will land closer to launch.

These gaps will be filled as the launch approaches, and they land first in our continuously updated Thomson Reserve review — the published site plan is already up there, with floor plans and pricing to follow.

Who will buy Thomson Reserve

The buyer pool is the second pillar of this project. Thomson Reserve sits at the intersection of five demand streams, which is why the site has been called the "blockbuster of 2026" since the en bloc cleared.

The biggest single group is HDB upgraders from Bishan, Ang Mo Kio, Toa Payoh, and Thomson. Deep HDB stock hits MOP continuously here. The 3BR at $2.5M-$2.7M is achievable on a combined $18K-$22K income, with HDB equity covering a meaningful down payment. It is the same upgrader stream that keeps resale moving at The Panorama beside Mayflower MRT, where the 3-bedroom trades at a $2.22M median.

Landed downgraders from the surrounding Upper Thomson and Sembawang Hills enclaves come next, looking for lift access, facilities, and security. They target the 4BR and 5BR at $4M-$4.5M as a realistic swap for a $5M-$7M older landed sale; PSF matters less, views and orientation more.

Retirees right-sizing from larger condos make up a smaller but consistent slice. They target 3BR and 4BR, mostly cash or minimal financing, prioritising quality and facilities over yield.

TEL-driven investors are the next stream. Upper Thomson to Orchard is roughly 10 minutes, Marina Bay 17. A 2BR at around $1.84M with $4,500-$5,000 a month in rent works to a 3.0-3.3% gross yield. The 1BR math is tighter but more liquid.

Younger professional couples in their early 30s, trading up from a first HDB, will look at the 2BR and compact 3BR. They are the price-sensitive segment and will compare directly against Lentor, River Valley, and Bayshore launches.

No single profile carries the launch. Thomson Reserve works because five profiles compete for the same stock, which is why the exit demand stays deep across cycles.

Best units by buyer profile

Since floor plans and the unit mix are not yet public, the guidance below is directional: which unit type is likely to fit each profile, subject to layout confirmation when the floor plans drop.

Solo or couple, no kids: 1BR and compact 2BR. Baseline $1.21M-$1.27M for 1BR, $1.75M-$1.84M for 2BR. Widest rental exit pool. Watch for 1BR layouts under 450 sqft.

Couple planning ahead: 2BR+Study. Flex-layout where study converts to nursery within 3-5 years. Expected $1.85M-$2.10M.

Young family with one kid: compact 3BR (around 900 sqft). Ai Tong within 1km is the decisive amenity. Baseline $2.25M-$2.50M. Key check at floor plan release: is the second bedroom 9 sqm or larger?

Established family (2-3 kids): 3BR standard (around 1,000 sqft) or 4BR. Baseline $2.50M-$3.25M. Three-kid families need 4BR or 3BR+Study; the 3BR standard will feel tight.

Multi-gen or large family: 5BR at $4.25M-$4.50M baseline, potentially $4.90M. Competition from landed downgraders means launch-day stack selection matters more than any other tier.

Investors on yield: 1BR or compact 2BR. 1BR at $1.21M-$1.27M with $3,500-$3,800/month rent works to 3.4-3.8% gross yield.

Watch-out: 4BR north of $3.5M stretches the exit pool. Landed downgraders absorb it, upgraders cannot.

Provisional; will be re-assessed when floor plans and actual pricing are public.

Reasons why Thomson Reserve might not be for you

Being honest about the trade-offs matters more on a blockbuster launch than on a quiet one, because hype tends to paper over the real constraints.

If you need parking for the Shunfu and Soo Chow food scene. The eateries across the junction from Upper Thomson MRT (Mingfa noodles, the roti prata house, the salted caramel place, Soi 90 Thai) are good, but parking is genuinely a pain. Street parking is limited and the coffeeshop lots fill up fast on weekends. If your weekend routine involves driving to these food spots with family, Thomson View is actually better as a walk-over project than a drive-to project. That is fine for most buyers, but if your lifestyle is car-dependent, factor it in.

If you drive home between 6pm and 8pm. Upper Thomson Road outside Thomson Plaza snarls every weekday for the full evening peak, and the Bright Hill Drive corridor compresses with it. Adding 1,240 households to the area will make it worse. If you commute by MRT this is moot; if you drive home in peak, it isn't.

If you are buying the far-end stacks at MRT doorstep pricing. Stack selection is going to matter more at Thomson Reserve than at most launches because the plot is elongated. The closest stacks to Upper Thomson MRT are a 1-minute covered walk. The far stacks are a 6-8 minute walk. If the developers charge "MRT doorstep" premium across all stacks equally, the far stacks are the weaker buy at that tier. Watch how the stack premiums are structured when the pricing is released.

If you are worried about the launch price landing above the baseline. The developer math has a range, and the range includes outcomes above $2,800 psf. If that happens, the upgrader pool for the 3-bedroom tier gets compressed and the exit risk rises. This is the single biggest variable in whether Thomson Reserve is a low-risk buy or a tighter one.

Thomson Reserve preview QPE: 8/10, Price pending

Thomson Reserve scores 8/10 on our preview assessment: Quality 4/4, Exit 4/4, and the Price pillar held until official pricing lands.

Quality 4/4. 504,000 sqft of elevated ground in D20, among the rarest plot sizes any Singapore condo will see this decade. UOL-SingLand-CapitaLand is the closest thing to a maximum-strength delivery consortium in the country. Upper Thomson MRT at the doorstep, Bright Hill MRT as walkable alternative, Marymount MRT on the CCL within reach. Ai Tong School inside the 1km priority zone. Elongated south-facing plot opens reservoir and landed views from upper floors.

Exit 4/4. The deepest buyer pool of any 2026 launch we have assessed. Five profiles competing for the same stock: HDB upgraders (primary), landed downgraders (4BR/5BR), retirees right-sizing (3BR/4BR), TEL-driven investors, younger couples. All five buyer pools want the same stock. Add Ai Tong, MacRitchie lifestyle, and Upper Thomson's 10-minute ride to Orchard.

Price: pending. The land cost ($1,178 psf ppr) points to a launch in the high-$2,000s psf, and Penrith's $2,800 average at near-identical land cost is a useful reference. But until the official price list is out, that is an estimate, not a rating. We score the Price pillar when the developers publish their numbers.

On what we can see today, the land, developers, schools and MRT are all in place. The open variable is the price. Price it keenly and this climbs toward a 9 or 10 out of 10; price it at the top of the range and it holds at 8 out of 10.

We will update this preview against the formal price sheet, and our continuously updated Thomson Reserve review carries the current call.

Data sources: Straits Times High Court collective sale reporting, EdgeProp Singapore property news, URA Realis, OneMap, PropertyGuru project listings, developer microsites, and internal on-the-ground observations of the site and surrounding amenities.

Published by MJ Review Homes (reviewhomes.sg) | PropNex Realty Pte Ltd | Shaik Amar R058640H | Myra Jalil R058979B | +65 9690 5440 | +65 9738 3705

Thomson Reserve (Thomson View site) at Bright Hill Drive

District 20 — Upper Thomson MRT at the doorstep

Tap or hover over any dot for details