A SingHaiyi-led consortium has acquired Loyang Valley for $880 million on its third en bloc attempt — $940 psf ppr after factoring in land betterment charges and the lease upgrading premium. Applying our land cost formula, starting launch pricing points to around $2,100 psf, with the development likely averaging $2,200 to $2,400 once the full unit mix plays out. The 840,648 sq ft site can yield roughly 1,249 units, making this the second-largest residential redevelopment in the east after Mandarin Gardens.

Source: Streetdirectory.com

Source: Streetdirectory.com

Loyang Valley Sold: Third Time Lucky

Loyang Valley has been sold collectively for $880 million to a consortium led by SingHaiyi Group — the largest successful collective sale of 2026, and the first major en bloc to clear since the rear block of The Centrepoint went for $391.9 million in February. The deal closed on April 17, 2026, capping a 10-week private treaty window that followed a February tender close. It was brokered by Terence Lian, head of investment sales at Huttons Asia, with Lee Liat Yeang at Dentons Rodyk acting for the buyers.

This was Loyang Valley's third attempt at collective sale. On the third try the reserve held at $880 million — the same figure the site was relaunched at on January 8 — and a buyer stepped up before the private treaty ran out.

For buyers watching Pasir Ris, this is the starting gun on what will likely become the area's largest new private residential launch in years — and arguably a product class this stretch of the east does not currently have. At 840,648 sq ft, the site is the second-largest residential plot in the east after Mandarin Gardens at 1.08 million sq ft, with room for up to 1,249 units under Draft Master Plan 2025. Scale of that kind gives the developer real design latitude — proper facility footprint, genuine block separation, landscape density, resort-style amenity architecture — the kind of project this part of Pasir Ris does not have today. That pulls in demand from buyers who want large-scale, amenity-rich living in the east and currently cannot find it here.

How We Review: The QPE Framework

Every review on this site runs through our QPE framework — Quality, Price, Exit.

Quality covers developer track record, land size, layouts, MRT access, views, and facilities. Price examines total price (not psf) and how it compares against what the market has tested — is there a price gap, or are you paying above proven territory? Exit asks who buys from you when it is time to sell, what the demand pool looks like, and what competing supply exists at resale.

At GLS stage, the focus narrows. There are no floor plans, no sales gallery, no indicative pricing — only land cost and location fundamentals. We rate downside risk as "not rated" at this stage: no benchmark exists yet to measure entry against.

Loyang Valley's $880M Deal in Numbers

The headline price of $880 million is only part of the story. Factor in an estimated $226 million in land betterment charges and a $246 million lease upgrading premium, and the effective land cost works out to $940 psf per plot ratio (psf ppr). That is the number to anchor on.

| Component | Amount |

|---|---|

| Collective sale price | $880 million |

| Land betterment charges (estimated) | $226 million |

| Lease upgrading premium | $246 million |

| Effective land cost | ~$1.35 billion |

| Maximum gross floor area (GFA) | ~1,350,000 sq ft |

| Effective land cost | $940 psf ppr |

| Potential unit yield | ~1,249 units |

Source: EdgeProp, Huttons Asia tender data, Draft Master Plan 2025.

A few details worth pulling out:

- The Loyang Valley site carries a 99-year lease from 1982 — about 55 years remaining. The $246 million lease upgrading premium resets that to a fresh 99-year lease for the new development.

- The Civil Aviation Authority of Singapore granted an uplift to the height limit in August 2025, from 40 m to 50 m. That opens up to 12 storeys of redevelopment, meaningfully more than the existing 4-to-7-storey blocks.

- Existing owners walk away with proceeds ranging from $1.67 million ($1,668 psf) for the smallest 1,001 sqft unit to $3.91 million ($1,195 psf) for the largest 3,272 sqft unit — a meaningful uplift over 2025 resale caveats that ranged from $1.08 million to $1.9 million.

Gallant Tang, SingHaiyi's 30-year-old group CEO, called the site "anchored by strong East Coast fundamentals" with "clear, compelling long-term potential." He also flagged the 840,000 sq ft footprint as "a rare opportunity to create a distinctive living concept." The scale rhetoric is not marketing fluff — there are only a handful of private sites this large available in the east, and Mandarin Gardens is the only bigger one.

Loyang Valley Launch Price: $940 PSF Explained

Our land cost formula applies three multipliers on top of raw land cost: 72% for development costs, 8% harmonised adjustment, and 20% developer margin. Total multiplier: 2.23x for a starting launch PSF, 1.86x for breakeven. On $940 psf ppr of land cost:

| Layer | Running PSF | What it represents |

|---|---|---|

| Land cost | $940 | Tender + LBC + LUP |

| + 72% development costs | $1,617 | Construction, fees, marketing, financing |

| + 8% harmonised | $1,748 | Breakeven |

| + 20% margin | $2,096 | Starting launch PSF (~$2,100) |

Source: reviewhomes.sg land cost formula (land cost × 2.23 = starting launch PSF).

That $2,100 psf is a floor — where the most affordably positioned stack or lowest-floor unit might start. Real launch averages typically run 5-10% higher once the premium floor bands, larger units, and rarer layouts are priced in. The likely settlement range: starting around $2,100 psf, averaging $2,200-$2,400 psf across the development.

Translated into total prices by unit size:

| Unit type | Starting (~$2,100 psf) | Likely average ($2,200-$2,400 psf) |

|---|---|---|

| 1-bedroom (~500 sqft) | ~$1.05M | ~$1.10M - $1.20M |

| 2-bedroom (~700 sqft) | ~$1.47M | ~$1.54M - $1.68M |

| 3-bedroom compact (~900 sqft) | ~$1.89M | ~$1.98M - $2.16M |

| 3-bedroom (~1,000 sqft) | ~$2.10M | ~$2.20M - $2.40M |

| 4-bedroom (~1,200 sqft) | ~$2.52M | ~$2.64M - $2.88M |

Source: reviewhomes.sg projections based on $940 psf ppr land cost. Actual pricing depends on SingHaiyi's final unit mix and stack strategy.

One corroborating signal: when SingHaiyi priced Vela Bay in Bayshore on April 9, they landed 10% below their own GLS land cost projection — pricing 1BR-to-3BR Premium stacks at a $2,500 starting PSF despite the $1,388 psf ppr land cost. If the same pricing discipline carries to Loyang Valley, the starting tier could come in softer than the formula suggests. We are not going to bet on that — starting around $2,100 psf remains the honest floor. But the softer scenario stays in the frame.

Why SingHaiyi Paid Up

SingHaiyi is not new to large-scale redevelopment. Track record:

- Parc Clematis (1,468 units, Clementi) — built on the former Park West site that SingHaiyi bought en bloc for $840.9 million in January 2018. Fully sold, completed 2023.

- Grand Dunman (1,008 units, District 15) — launched July 2023. About 90% sold at an average $2,518 psf as of April 2026. One of the largest-scale D15 launches of its cohort.

- Vela Bay (515 units, Bayshore) — Gallant Tang's first project as SingHaiyi CEO. The sales gallery drew nearly 8,000 visitors over its April 11-12 debut weekend, with confirmed pricing released a week later. Launch was slated for April 25.

Loyang Valley is Tang's first en bloc deal since stepping into the CEO role. The thesis is consistent with Vela Bay: large-plot redevelopment in an east-side corridor with coming MRT infrastructure. Two big projects in the east in the same 12-month window, from the same developer, with the same scale-and-amenities play.

For buyers, the relevant signal is pipeline discipline. SingHaiyi's recent launches have cleared at high absorption, and the Vela Bay pricing approach suggests they are willing to price to the market rather than push the land cost ceiling aggressively.

What Surrounds the Loyang Valley Site

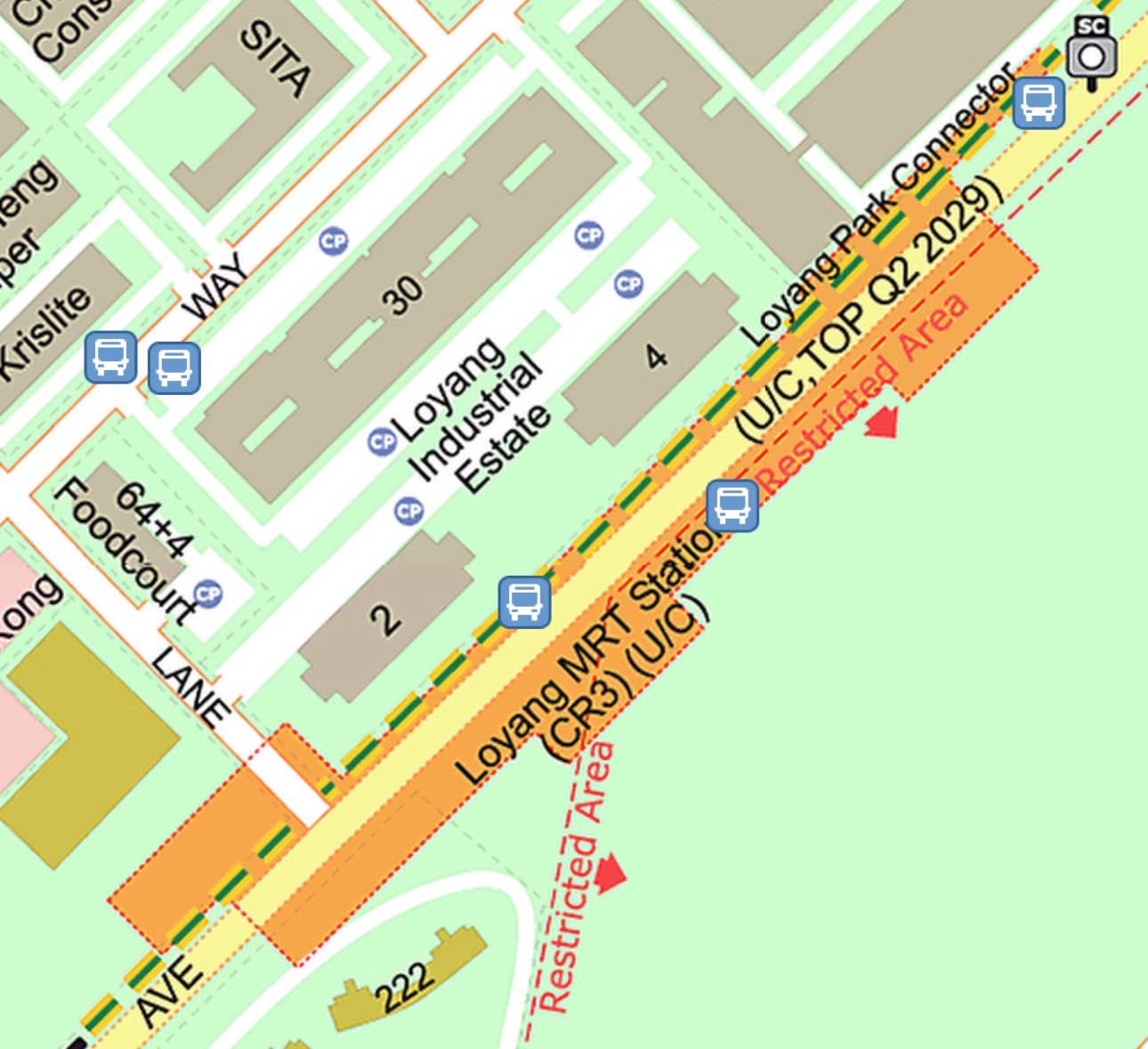

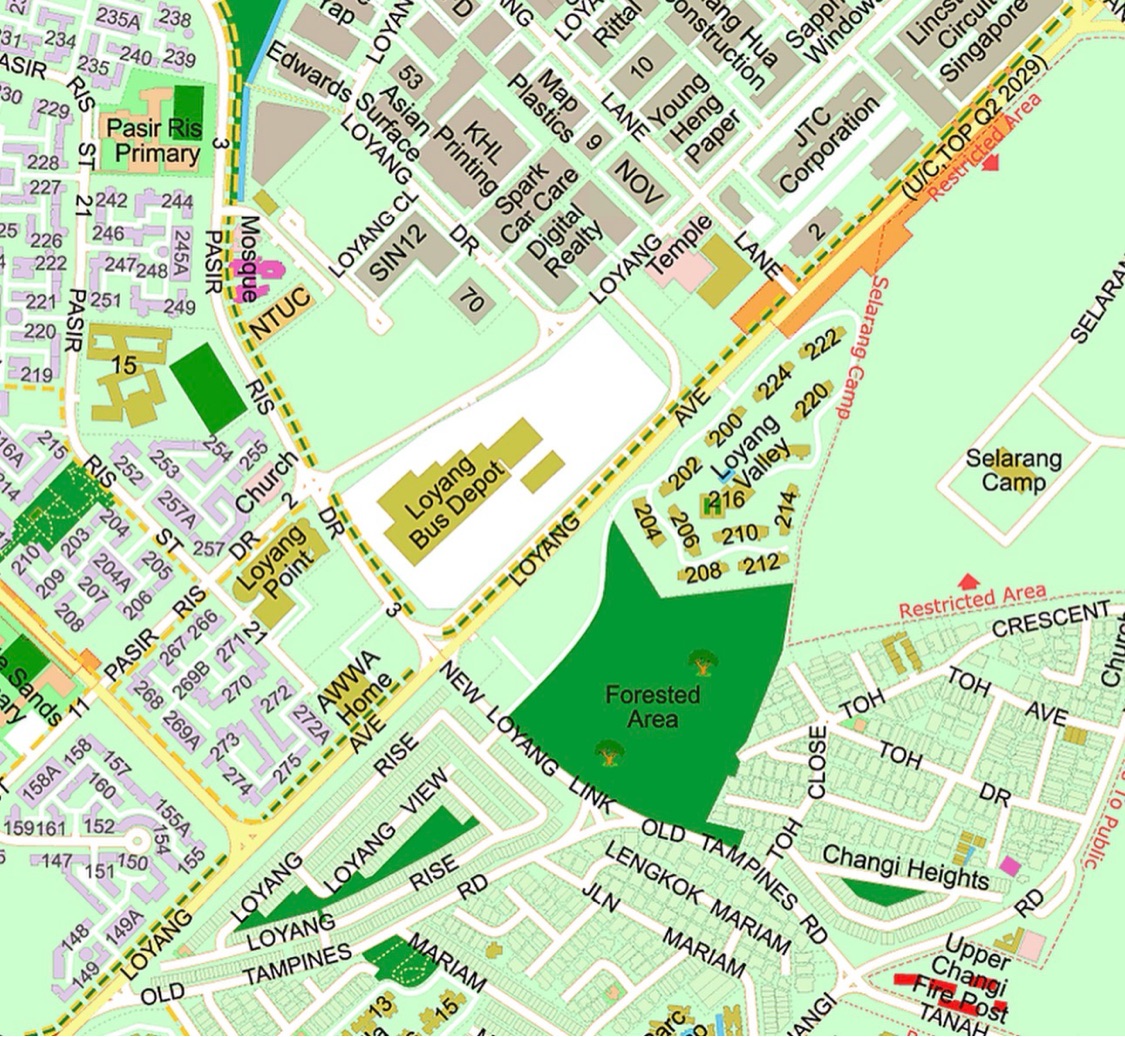

Future Loyang MRT (CR3). The Cross Island Line's Loyang station will sit directly underneath Loyang Avenue at its junction with Loyang Lane — roughly 450 m from the Loyang Valley entrance. URA's construction map lists it as TOP Q2 2029 as part of CRL Phase 1. The redevelopment's TOP timeline — typically 3-4 years from tender — lands after the MRT opens, so the first residents move in to a site that is already a short walk from the train.

Source: URA OneMap

Source: URA OneMap

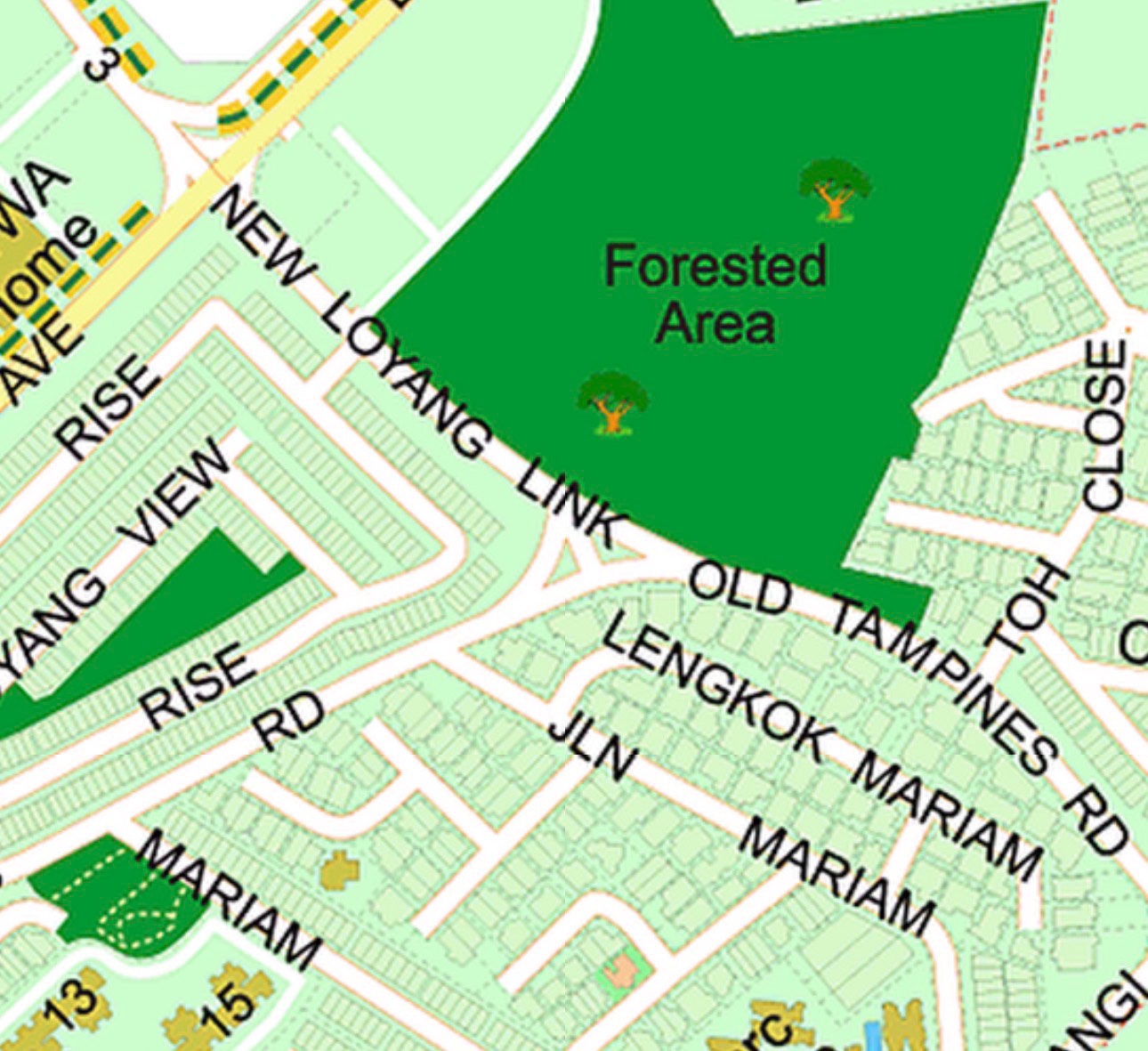

Unblocked on all four sides. The plot sits surrounded entirely by low-rise. South and south-east: a protected forested reserve, then landed housing along Jalan Mariam, Lengkok Mariam, Loyang View Rise, and Changi Heights. East: Selarang Camp, an active SAF military base that essentially cannot rezone. West: Loyang Bus Depot. North: light-industrial buildings of Loyang Industrial Estate across Loyang Avenue. For a 1,249-unit redevelopment, that is rare. South and east-facing stacks get genuinely premium, structurally protected views — forest and military land rarely rezone in Singapore. North and west stacks are unblocked too, though the views are industrial and utility respectively, and the developer will likely price those edges more conservatively.

Source: URA OneMap

Source: URA OneMap

Source: URA OneMap

Source: URA OneMap

Loyang Point for daily convenience. The Loyang Point neighbourhood mall sits just across Loyang Avenue from the site, anchoring day-to-day retail, F&B, and convenience needs until the CRL opens and the upgraded corridor lands.

Primary schools within 1km. Huttons cites two primary schools inside the 1km P1 priority zone. The closest Pasir Ris cluster schools — Casuarina Primary (which absorbed the former Loyang Primary in the 2019 MOE merger), Elias Park Primary, and Pasir Ris Primary — are the likely candidates. Parents planning around P1 should verify against MOE's school finder once the block-level site plan is published.

Changi Northern Corridor. The Loyang Viaduct completes in 2028, with the full corridor — including widening Loyang Avenue to Aviation Park Road from dual 2-lane to dual 4-lane — done by 2030. That improves both commute time and expressway access for the whole Pasir Ris-Loyang corridor.

Changi Airport Terminal 5. The long-term employment driver. T5 construction is underway, and Changi East is the regional aviation hub. For buyers working in aviation or the wider Changi business district, the site is a 10-minute drive to their desks. Pasir Ris Park, Downtown East, and the beach sit within a short drive to the north.

The Pasir Ris Cluster at Launch

By the time Loyang Valley launches — likely 2027 or 2028 — the Pasir Ris cluster will look different from today. For context on what's currently in play:

| Project | Status | Price signal |

|---|---|---|

| Pasir Ris 8 | TOP June 2026 | Subsale avg $2,050 psf, high $2,200 psf (Dec 2025) |

| Coco Palms | Resale, TOP 2019 | Avg ~$1,655 psf |

| Coastal Cabana EC | Recently launched | EC launch pricing (materially below private condo PSF) |

| Loyang Valley (future) | GLS — launch 2027/28 | Projected starting ~$2,100 psf, avg $2,200-$2,400 |

Source: reviewhomes.sg cluster tracker, URA Realis caveats, newlauncher.com.sg data.

Pasir Ris 8 is the direct psf benchmark today. At $2,050 average and $2,200 at the high end, the integrated MRT premium is what buyers are paying for — and Loyang Valley will not have that. What Loyang Valley will have is structural: significantly more land (840,648 sqft vs 95,584 sqft at Pasir Ris 8), a fresh 99-year lease, facility density that a 487-unit integrated tower simply cannot match, the CR3 Loyang MRT station on its doorstep from Q2 2029, and unblocked views on every side — south- and east-facing stacks looking out over a forested reserve and an SAF military base whose land use is essentially locked in.

These are fundamentally different products, not two variants of the same thing. Pasir Ris 8 is for the buyer who prioritises zero-metre MRT integration and will pay the premium for it. Loyang Valley is for the buyer who wants scale — proper facility architecture, genuine block spacing, landscape density, the full large-site experience — and is willing to take a 450 m walk to the future MRT in exchange. That buyer currently has nowhere to land in the Pasir Ris corridor. Large-scale redevelopments of this kind exist in other parts of the island — Grand Dunman in District 15, Parc Clematis in Clementi — but not in the Pasir Ris-Loyang stretch of the east. Loyang Valley fills that gap, and the demand pool it attracts barely overlaps with what's currently in play here.

For a fuller view of the cluster, see our Pasir Ris condo guide.

Where Loyang Valley Prices Likely Settle

Starting launch PSF: ~$2,100. Likely average: $2,200-$2,400. A 3-bedroom around 1,000 sqft probably opens near $2.10M and lands $2.20M-$2.40M once the full stack is priced.

Three factors tilt the average toward the upper end of that range. First, SingHaiyi paid $940 psf ppr — not a soft number — and will want a margin on that. Second, the site is unblocked on all four sides, with structurally protected views to the south (forested reserve + landed) and east (Selarang Camp SAF land). That gives the developer whole blocks of view-premium stacks to price up, not just the top-floor minority. Third, the scale creates its own demand pool — buyers who want a large, amenity-rich project in Pasir Ris currently have no comparable option, and that demand supports firmer pricing than a pure "cheaper than Pasir Ris 8" comparison would suggest.

What to watch between now and launch:

- Unit mix announcement. The 1,249-unit yield assumes 100 sqm average. A tilt toward smaller units pulls the entry price closer to $1.5M territory; a tilt toward larger family units pushes the average higher. The mix tells you who the developer is targeting.

- Sales gallery timing. Typical redevelopment timeline runs 18-24 months from tender award to preview. A late-2027 or 2028 preview is realistic.

- Cross Island Line progress. Loyang MRT is currently listed as TOP Q2 2029 on URA's construction map. If that slips or accelerates, the walk-to-MRT access at launch shifts with it.

- SingHaiyi's pricing discipline. Vela Bay priced 10% below its land cost projection. If the same approach carries over, starting pricing could land closer to $1,900-$2,000 psf at the floor.

For buyers today: this is a watch-list site, not a buy-now call. Get the floor plans when they drop. See the unit mix. See where indicative pricing lands. The QPE verdict comes at launch — not at land tender.

Data sources: EdgeProp (Loyang Valley en bloc sale, 17 April 2026), Huttons Asia tender data, Draft Master Plan 2025, URA Realis, Land Transport Authority (Cross Island Line), Ministry of Education (school registration zones), reviewhomes.sg land cost formula.

Loyang Valley redevelopment site

District 17 — 840,648 sq ft along Loyang Avenue, between the future Loyang MRT and Pasir Ris MRT

Tap or hover over any dot for details

All information provided is for general reference only and is based on current planning assumptions. Details are subject to change without notice and may vary depending on final design development, regulatory requirements, and operational considerations. No representation or warranty is made as to the accuracy or completeness of the information provided.